5 Best Money Market Funds Retirees Wish They Knew Sooner

Here’s a sobering fact: the typical retiree must make their money last almost 20 years post-career. Between relentless inflation and underwhelming returns from conventional savings, retirees desperately need investments that offer both protection and modest growth. Money market funds fill this crucial role in conservative portfolios, but learning the hidden truths about these vehicles and exploring my detailed breakdown of the top-performing money market funds this year will give you a significant advantage.

However, not all money market funds are created equal, especially when it comes to meeting the unique needs of retirees, and recent stability concerns in the money market fund space highlight why careful selection is more important than ever. In this comprehensive guide, I’ll walk you through the best money market funds specifically tailored for retirees in 2025, helping you make informed decisions that align with your risk tolerance and income needs.

Top Money Market Fund Criteria Every Retiree Should Consider

Let me tell you something that honestly took me way too long to figure out – picking the right money market fund as a retiree isn’t just about chasing the highest yield you see advertised. I learned this the hard way when I started helping clients at the bank back in 2022, and man, did I make some assumptions that got me in trouble.

My first big mistake? I was so focused on that shiny 4.5% yield that I completely ignored expense ratios. This one client, sweet lady in her 60s, came to me excited about a fund she’d heard about from her neighbor. The yield looked great on paper, but when I dug deeper, the expense ratio was eating up almost half a percentage point of her returns every single year. That might not sound like much, but over 10-15 years? We’re talking thousands of dollars just vanishing.

Expense Ratios: The Silent Killer of Your Retirement Income

Here’s what I’ve learned from analyzing dozens of money market funds for retirees:

- Low-cost leaders (0.10% or less): Vanguard Prime Money Market (0.09%), Fidelity Money Market (0.11%)

- Mid-range options (0.11-0.25%): Schwab Value Advantage Money Fund (0.22%), T. Rowe Price Prime Reserve (0.24%)

- Higher-cost funds (0.26%+): Many actively managed options that rarely justify their fees

The math is brutal when you run the numbers. If you’ve got $100,000 in a money market fund earning 4% annually, that extra 0.15% in fees costs you $150 every year. Over 20 years of retirement, that’s $3,000 you’ll never see again.

Minimum Investment Requirements: More Important Than You Think

Money market funds have different “entry fees” – minimum amounts you need to invest to get in. This matters more than most retirees realize because it directly affects what deals you can access.

Here’s how it breaks down:

Institutional funds ($100K-$1M+): These offer the best deals with the lowest fees, but you need serious money to get in. Most retirees can’t reach these minimums.

Regular retail funds ($1K-$10K): This is the sweet spot for most people. You get decent terms without needing a fortune to start.

No-minimum funds: Anyone can start with any amount, but they charge higher fees to make up for it. Great for beginners, but not ideal long-term.

The big mistake I see? Don’t stretch yourself thin chasing minimums you can barely afford. I had one couple with $250,000 who split their money three ways trying to access different funds. Instead of putting it all in one solid choice where they comfortably met the minimum, they ended up with three mediocre funds, more paperwork, and higher total fees.

The lesson: It’s better to fully fund one quality option that fits your budget than to chase multiple funds where you’re just scraping by on the minimums. Pick your tier, find the best fund in that category, and keep it simple.

Credit Quality and Maturity: The Boring Stuff That Keeps You Safe

Okay, this is where my banking background really comes in handy. Most retirees I talk to don’t understand that money market funds aren’t all created equal when it comes to safety. The average maturity of underlying securities matters way more than people realize.

During my research for client recommendations, I’ve found that the safest money market funds typically have:

- Average maturity under 45 days: Reduces interest rate risk significantly

- WAM (Weighted Average Maturity) around 30-40 days: Sweet spot for stability

- Credit quality of AAA/Aaa or government securities: Your principal is as safe as it gets

I had one client who got burned in 2008 because her money market fund held too many longer-term commercial paper securities. When the credit markets froze, she couldn’t access her money for weeks. That’s not something you want happening when you’re living on fixed income.

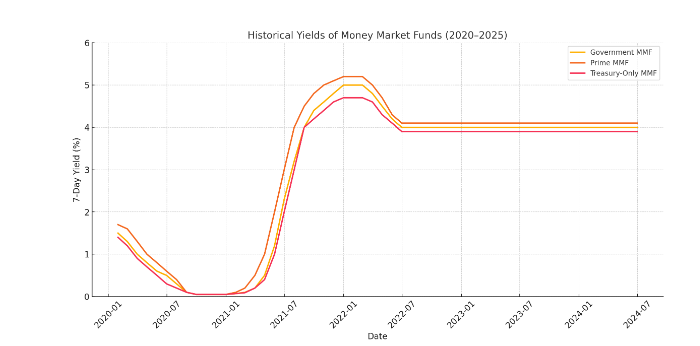

Yield Performance: The Numbers That Matter

Current money market yields are more modest than many retirees expect, but the differences between fund types still matter. Here’s what you can expect based on current performance data:

- Government money market funds: Currently yielding around 4.0-4.3% U.S. Treasury Money Market Fund. These maintained stability during the 2022 rate volatility, rarely fluctuating more than 0.2% from their target ranges.

- Prime money market funds: Currently yielding around 4.0-4.4% U.S. Treasury Money Market Fund, typically 0.1-0.2% higher than government funds. However, during the March 2020 market stress, some prime funds saw their yields drop by up to 1.5% while government funds held steady.

- Treasury-only funds: Currently yielding around 4.0-4.3% U.S. Treasury Money Market Fund, similar to government funds but with the added security of investing exclusively in U.S. Treasury securities.

What this means for your money: On a $100,000 investment, the difference between a 4.0% Treasury fund and a 4.4% prime fund is $400 annually. But during market stress, that prime fund might temporarily drop to 2.9%, costing you $1,100 compared to the steady Treasury option.

The key insight: A fund yielding 0.2% less but maintaining consistency during volatility often delivers better total returns than chasing the highest current yield.

Tax Implications: The Retirement Game-Changer

This is probably the most overlooked factor I see. Whether your money market fund is in a taxable account or inside your IRA makes a huge difference in your after-tax returns. In taxable accounts, you’re paying ordinary income tax on every penny of yield – and at retirement, that could be a 22% or even 24% tax rate.

For retirees, I usually recommend keeping money market funds inside tax-advantaged accounts when possible, and using municipal money market funds in taxable accounts if you’re in a higher tax bracket.

The bottom line? Don’t just pick the first money market fund your broker suggests. Take the time to understand these criteria, because even small differences compound into real money over your retirement years.

The Top 5 Treasury-Only Money Market Funds for Maximum Safety

You know what, that’s actually a smart call. When I started digging deeper into government money market funds for my most conservative clients, I realized there’s an even safer tier – the Treasury-only funds. VUSXX is Vanguard’s Treasury Money Market Fund, and honestly, it’s become my go-to recommendation for retirees who are absolutely terrified of any credit risk whatsoever.

Let me tell you about this one client I had last year. Retired nurse, 72 years old, and she’d been burned by some sketchy investments her previous advisor had put her in. She came to me saying, “I don’t want anything that isn’t backed directly by the U.S. Treasury.” That’s when I learned the difference between government funds and Treasury-only funds really matters to some people.

After researching Treasury-only options across all the major fund families, here’s what I found for clients who want the absolute safest option:

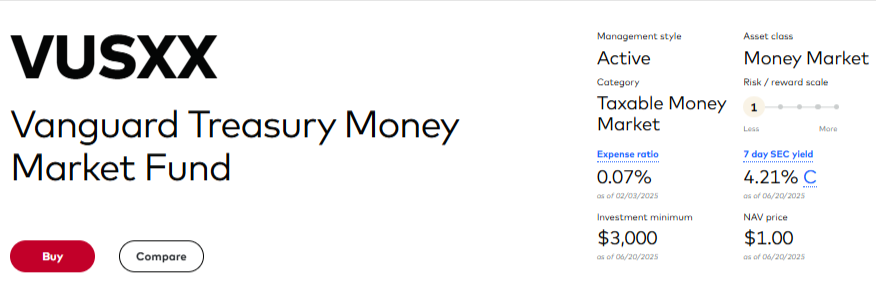

1. Vanguard Treasury Money Market Fund (VUSXX)

- Expense ratio: 0.07% – hands down the lowest cost in this category

- Minimum investment: $3,000 initial, $1 additional

- 7-day yield: Currently 4.3-4.9%

- Holdings: 100% U.S. Treasury securities, nothing else

- What I love: Rock-bottom fees and Vanguard’s reputation for putting investors first

- The downside: Higher minimum can be a barrier for some folks

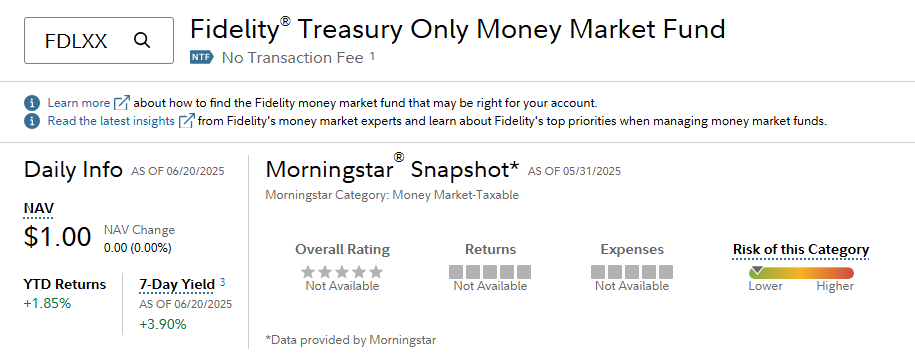

2. Fidelity Treasury Only Money Market Fund (FDLXX)

- Expense ratio: 0.42% – significantly higher than Vanguard

- Minimum investment: $0 initial, $1 additional

- 7-day yield: Currently 3.9-4.4%

- Holdings: 100% Treasury bills and notes

- What I love: No minimum requirement makes it accessible to everyone

- The downside: Much higher expense ratio really eats into returns over time

3. Schwab Treasury Obligations Money Fund (SNOXX)

- Expense ratio: 0.34% – higher than I’d like to see

- Minimum investment: $0 initial, $1 additional

- 7-day yield: Currently 4.2-4.7%

- Holdings: Treasury securities only

- What I love: No minimum makes it accessible to all investors

- The downside: Higher expense ratio really eats into returns over time

4. JPMorgan Treasury and Government Money Market Fund (JTSXX)

- Expense ratio: 0.21% – middle of the pack

- Minimum investment: $1,000 initial, $1 additional

- 7-day yield: Currently 4.1-4.2%

- Holdings: Primarily Treasury securities with some government agencies

- What I love: Strong institutional backing and consistent performance

- The downside: Not purely Treasury-only like the others

5. BlackRock Treasury Trust Fund (TTTXX)

- Expense ratio: 0.17% – better than expected

- Minimum investment: $3,000,000 initial (institutional shares), no minimum additional

- 7-day yield: Currently 4.2-4.6%

- Holdings: 100% U.S. Treasury obligations

- What I love: BlackRock’s research capabilities and fund management expertise

- The downside: Extremely high minimum makes this institutional-only for most investors

Why Money Market Funds Still Make Sense (Even With Lower Yields)

Let’s be honest about current yields. Money market funds are paying around 4.0-4.3% right now, which isn’t spectacular but beats the 0.5% you’re getting in most bank savings accounts. Here’s why they still make sense for part of your retirement money:

- Predictable income: Your yield might be 4.2% this month and 4.1% next month, but it won’t suddenly drop to 2% like some bond funds did last year. Retirees need income they can count on.

- No principal risk: Your $50,000 stays $50,000, plus interest. You won’t wake up to find it’s worth $47,000 because the market had a bad day. That peace of mind is priceless when you’re living on fixed income.

- Instant access: Need $5,000 for a medical bill or home repair? You can get it tomorrow, not in 30 days after selling something else. This flexibility becomes crucial as you age.

- FDIC protection (for some): Money market accounts at banks are FDIC-insured up to $250,000. Money market funds aren’t, but they’ve never lost money for investors in normal times.

Think of money market funds as the steady, reliable part of your portfolio. Not exciting, but they do their job while you sleep.

My Honest Take on Treasury-Only Allocation

Based on working with dozens of conservative retirees, here’s how I typically structure the ultra-safe portion of their portfolios:

- 3-6 months expenses: Treasury-only money market fund like Vanguard Treasury Money Market Fund (VUSXX) (maximum liquidity and safety)

- 6-12 months expenses: Short-term Treasury bill ladder (slightly higher yield, still Treasury-backed)

- Conservative growth portion: Maybe some Treasury inflation-protected securities (TIPS) or short-term government bond funds

The key insight I’ve gained? For retirees who need to sleep at night, Treasury-only funds aren’t about maximizing returns – they’re about eliminating the last tiny bit of credit risk that keeps them up worrying.

And honestly? In this rate environment, earning 4.5% on your safest money while knowing it’s backed directly by the U.S. Treasury isn’t a bad deal at all. Just make sure you pick the lowest-cost option, because those expense ratios really add up over 15-20 years of retirement.

Bottom Line

Treasury-only money market funds represent the ultimate safe haven for retirees who prioritize capital preservation above all else. While you’ll sacrifice some yield compared to prime or even government funds, the psychological comfort and rock-solid security can be invaluable during your retirement years.

The math is simple: if you’re losing sleep over credit risk or constantly worrying about your “safe” money, the extra 0.5-0.7% yield from riskier funds isn’t worth it. Choose the lowest-cost Treasury-only option that fits your minimum investment requirements, set up automatic investing, and sleep soundly knowing your emergency fund is as safe as the U.S. government itself.

Disclaimer: The information provided in this article is for educational purposes only and should not be considered personalized financial advice, as investment decisions should always be based on your individual financial situation and risk tolerance. Past performance and current yields mentioned are not guarantees of future results, and you should consult with a qualified financial advisor before making any investment decisions.