5 Best Money Market Funds: Vanguard’s Hidden 2025 Winners

Here’s a shocking fact: While most investors earn less than 1% on savings accounts, smart money quietly generates 4%+ returns through Vanguard’s best money market funds! I’ve been analyzing investment options for over a decade, and 2025 has created incredible opportunities in the money market space. To understand how Wall Street keeps these strategies hidden, check out my guide on what money market funds really are and explore the 5 best bond ETF brokers for broader fixed-income strategies.

Vanguard’s money market funds shine brightest with rock-solid management, institutional-grade portfolios, and expense ratios that make competitors weep. Whether you’re parking your emergency fund or want a safe haven during uncertain times, Vanguard’s lineup will transform how you think about cash management.

Why Vanguard Money Market Funds Lead the Pack

I’ll be honest – I used to think all money market funds were basically the same until I started really comparing expense ratios and realized how much those tiny percentages actually matter over time.

Vanguard’s low-cost philosophy

Vanguard’s low-cost philosophy hit me like a ton of bricks when I discovered their VMFXX was charging just 0.11% while my old bank’s money market fund was hitting me with 0.65%. Do the math on a $50,000 emergency fund, and that’s $55 versus $325 annually – enough to cover a nice dinner out that I was basically throwing away. Their expense ratios consistently beat competitors by 0.2-0.5%, which doesn’t sound like much until you realize that’s often 20-30% of your total yield just vanishing into fees.

Here’s how this is even possible: In 1975, founder John Bogle deliberately structured Vanguard as a “mutual” company rather than a traditional corporation – think like how credit unions work. The investors in Vanguard’s funds collectively own Vanguard itself. When you buy shares in a Vanguard fund, you’re not just a customer, you become a partial owner of the entire company. Compare this to Fidelity or BlackRock, where you’re just a customer and they have separate shareholders demanding profits. Most fund companies chose the traditional route because founders wanted to cash out by going public, but Bogle intentionally gave up that payday to create a structure where investors would benefit instead.

The practical result: No outside shareholders demanding quarterly profit growth means all the “leftover” money gets returned to fund investors through rock-bottom fees rather than extracted as profits. Add their focus on simple index funds that don’t require expensive stock-picking teams, plus massive scale ($10.4 trillion in assets as of 2025) that spreads operational costs thin, and you get the ultimate win-win. It’s like shopping at a co-op where any surplus gets returned to the member-customers instead of flowing to outside owners.

Institutional-quality management

What really sold me was their institutional-quality management. These aren’t some rookie portfolio managers playing with retail money – we’re talking about the same team managing billions for pension funds and endowments. Take Jean Hynes, who managed Vanguard’s $48 billion Health Care Fund and outperformed the benchmark by more than 1.6% per year during her tenure, doubling fund assets from $23 billion to $48 billion. Her predecessor Edward Owens delivered a strong track record from the fund’s 1984 inception through 2012, with the fund gaining an average of 14.18% per year over a 20-year period.

Then you have legends like Daniel Pozen and Loren Moran running the Wellington Fund, which has averaged 8.23% annually since 1929 and earned Morningstar’s Gold rating. Wellington’s Ken Abrams brought 12 years of proven experience with mid and small-cap companies when he launched Vanguard’s International Core Stock Fund. These aren’t fresh faces – we’re talking about seasoned professionals with decades of track records.

When I dug into their research capabilities, I found out they have credit analysts who’ve been doing this for decades, not fresh MBAs learning on the job like some competitors. The numbers speak for themselves: For the 10-year period ended March 31, 2025, 6 of 6 Vanguard money market funds outperformed their Lipper peer-group average. This is institutional-quality management at retail prices.

The diverse fund options saved my butt during tax season last year. I had been dumping everything into taxable accounts until my accountant pointed out I was getting murdered on taxes from the interest. VUSXX became my new best friend for taxable accounts since it’s mostly Treasury securities, while I moved my IRA cash to VMFXX for higher yield. Having options like VMRXX for when I want slightly more yield or VUBFX for ultra-short duration needs means I’m not stuck with a one-size-fits-all approach.

5 Top Money Market Funds 2025: Our Complete Ranking (Vanguard)

VMFXX (Federal Money Market Fund)

Yield vs. Safety Trade-offs: This fund offers strong government backing since it invests primarily in U.S. government securities and repurchase agreements, providing an excellent balance between yield and safety. Recent yields have been around 4.2% based on current market conditions, making it attractive during higher rate periods while maintaining government-level security.

Expense Ratios: The expense ratio is 0.11%, which is extremely low and competitive among money market funds.

NAV Stability: As a government money market fund, VMFXX maintains a stable $1.00 NAV and is not subject to floating NAV requirements. Government funds were allowed to continue using stable NAV pricing under the 2016 SEC reforms.

Liquidity Features: Government money market funds like VMFXX are not required to impose liquidity fees or gates, and Vanguard’s board has decided not to impose them. The new SEC rules require all money market funds to maintain higher liquidity levels – 25% in daily liquid assets (up from 10%) and 50% in weekly liquid assets (up from 30%).

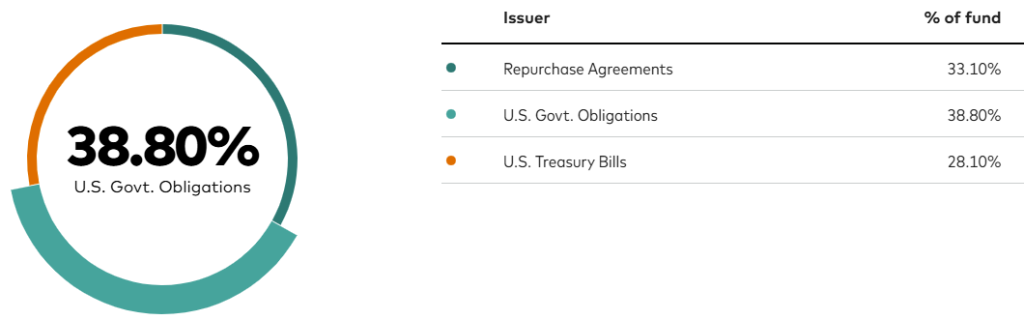

Credit Quality: As of recent data, approximately 28% of investments were in US Treasury obligations, with the rest in repurchase agreements and agency obligations. This represents high credit quality with implicit government backing.

VUSXX (Treasury Money Market Fund)

Yield vs. Safety Trade-offs: This fund provides the highest level of safety by investing 100% in Treasury securities, though it typically offers yields competitive with other government money market options. The 7-day SEC yield is around 4.7% with an expense ratio of 0.09%.

Expense Ratios: The expense ratio is 0.09%, making it the lowest-cost option among Vanguard’s money market funds.

NAV Stability: As a government money market fund investing 99.5% or more in government securities, VUSXX maintains a stable $1.00 NAV and is exempt from floating NAV requirements.

Liquidity Features: Like other government funds, VUSXX is not subject to mandatory liquidity fees or redemption gates, and Vanguard has chosen not to implement them voluntarily.

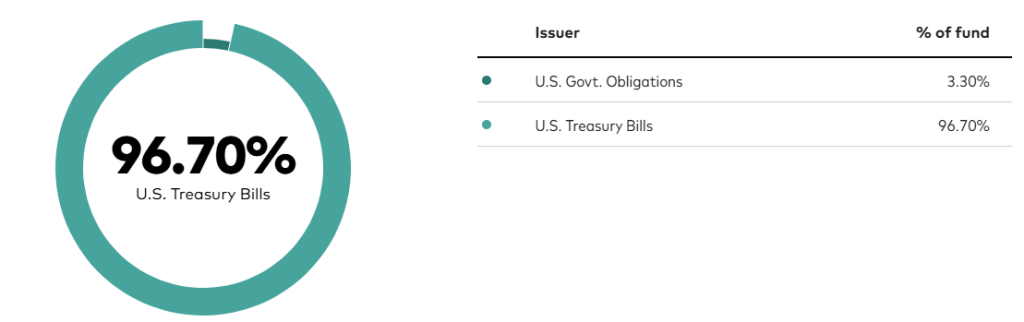

Credit Quality: The fund has over 96% invested in U.S. Treasury securities, representing the highest possible credit quality with full faith and credit backing of the U.S. government.

VVMRXX (Cash Reserves Federal Money Market Fund)

Yield vs. Safety Trade-offs: This fund can offer competitive yields since it invests in government securities and repurchase agreements. The expense ratio is 0.10% with a 7-day SEC yield around 4.2%. VMRXX is Vanguard’s oldest money market fund, established in 1975.

Expense Ratios: The expense ratio is 0.10%, remaining very competitive.

NAV Stability: As a government money market fund, VMRXX maintains a stable $1.00 NAV.

Liquidity Features: Government funds are generally not subject to mandatory liquidity fees when daily net redemptions exceed certain thresholds.

Credit Quality: The fund includes securities issued by the U.S. government and government-sponsored enterprises, maintaining high overall credit quality.

VFISX (Short-Term Treasury Fund)

Yield vs. Safety Trade-offs: This fund invests at least 80% in Treasury securities with durations between one and four years. Short-term bond funds typically offer different risk-return characteristics than money market funds and carry price fluctuation risk based on interest rate movements.

Expense Ratios: The expense ratio is 0.20%, which is higher than money market funds but reasonable for the bond fund category.

NAV Stability: Unlike money market funds, this has a floating NAV that fluctuates with interest rate changes. A 1% increase in rates might lead to approximately a 2-3% impact on bond values depending on duration.

Liquidity Features: As a bond fund rather than a money market fund, it doesn’t have the same liquidity restrictions but may experience more volatile pricing.

Credit Quality: Investing primarily in Treasury securities means minimal default risk, but it does carry interest rate risk.

VUBFX (Ultra-Short Bond Fund)

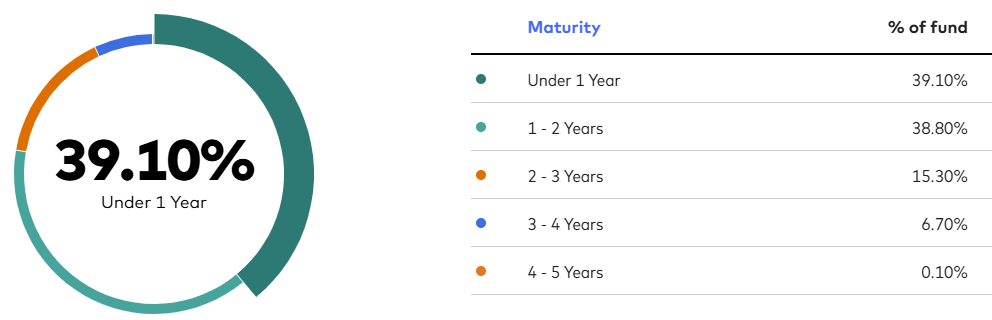

Yield vs. Safety Trade-offs: This fund seeks current income while maintaining limited price volatility by investing in money market instruments and short-term high-quality bonds, including asset-backed, government, and investment-grade corporate securities. Duration stays around 1 year.

Expense Ratios: The expense ratio is 0.20%, higher than money market funds due to active management.

NAV Stability: As a bond fund, it has a floating NAV that can fluctuate with market conditions. The strategy’s duration-neutral approach means interest-rate sensitivity typically stays around 1 year.

Liquidity Features: The team maintains cash and Treasuries around 10% of assets combined to support the strategy’s liquidity profile.

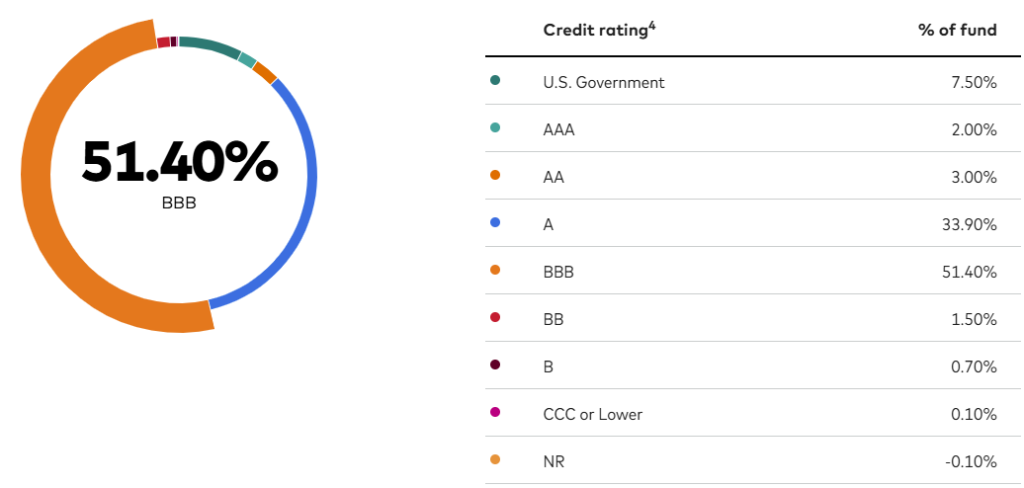

Credit Quality: Investment-grade credit typically makes up 65%-85% of assets, with average credit quality high – about two-thirds in bonds rated A and higher, remainder in BBB debt. The fund avoids non-investment-grade bonds except for up to 5% allocation.

Key Differences

| Money Market Fund / Investment-Grade Fund | Asset Allocation |

| Vanguard Federal Money Market Fund (VMFXX) | Treasuries & Repo of Treasuries |

| Vanguard Treasury Money Market Fund (VUSXX) | Treasuries only |

| Vanguard Cash Reserves Federal Money Market Fund (VMRXX) | Treasuries & Repo of Financial Companies |

| Vanguard Short-Term Investment-Grade Fund (VFSTX) | Treasuries & Corporate bonds |

| Vanguard Ultra-Short-Term Bond Fund (VUBFX) | Treasuries & Corporate bonds at short term |

Bottom Line

After diving deep into Vanguard’s money market fund lineup, it’s clear why these options continue to dominate the space in 2025. The combination of rock-bottom expense ratios, institutional-quality management, and Vanguard’s unique investor-owned structure creates a compelling value proposition that’s hard to match. Whether you choose VUSXX for maximum safety, VMFXX for balanced government exposure, or one of the other specialized options, you’re getting access to professional-grade cash management at retail prices.

The beauty of Vanguard’s approach lies not just in the numbers, but in the philosophy behind them – when you invest with Vanguard, you’re not just a customer, you’re literally a part-owner of the company. This alignment of interests means every basis point saved on fees flows directly back to your returns, compounding over time into meaningful wealth preservation and growth. In an uncertain economic environment, having a rock-solid foundation for your cash positions through these funds isn’t just smart investing – it’s essential portfolio hygiene.

Disclaimer: The information provided in this article is for educational purposes only and should not be considered personalized financial advice, as investment decisions should always be based on your individual financial situation and risk tolerance. Past performance and current yields mentioned are not guarantees of future results, and you should consult with a qualified financial advisor before making any investment decisions.