Treasury vs Corporate Bonds: Unlock Higher Returns Without Losing Sleep

Did you know that the U.S. bond market is worth over $50 trillion, making it nearly twice the size of the stock market? Yet many investors still struggle to understand the fundamental differences between Treasury and Corporate bonds!

If you’re wondering whether to invest in Treasury vs Corporate bonds, you’re not alone. I’ve spent years studying these fixed-income products, and the choice between these two bond types can significantly impact your portfolio’s performance and risk profile.

Whether you’re a conservative investor seeking stable income or someone willing to take on slightly more risk for higher returns, understanding the nuances between corporate and treasury bonds is crucial for making informed investment decisions. Let’s dive deep into this comparison and help you determine which bond type aligns with your financial goals.

What Are Treasury Bonds? (Government Securities Explained)

Treasury bonds first crossed my radar during childhood dinner table conversations, then resurfaced in my college finance courses as textbook theory. But the real education began when I stepped into my past role in Fixed Income Sales – suddenly, these weren’t just abstract concepts but the bread and butter of daily client conversations and market analysis. While most people don’t track Treasury bonds daily, they quietly influence everything from mortgage rates to credit card interest – making them worth understanding.

The Basics: What Treasury Bonds Actually Are

Treasury bonds are basically IOUs from the U.S. government. When you buy one, you’re lending money to Uncle Sam, and he promises to pay you back with interest. It’s that simple, though the mechanics can get a bit more complex.

The federal government issues these securities to fund everything from highway construction to military operations. Think of it as the government’s credit card, except instead of owing money to a bank, they owe it to regular folks like us. The Treasury Department handles all the paperwork and logistics through something called TreasuryDirect – their online platform that I wish I’d discovered years earlier.

The full faith and credit of the United States government backs every Treasury bond – a guarantee that carries the weight of a 200-year track record without a single default. This makes Treasuries the safest investment product you can buy, but I’ve grown increasingly concerned about the government’s mounting debt levels and whether they’re sustainable long-term. Sure, the Treasury can always print more money or raise our taxes to meet their obligations, but I see both options as passing the cost directly to us through inflation or heavier tax burdens.

The Treasury Security Family Tree

Here’s where I made my first big mistake – I thought all Treasury securities were the same thing. Turns out there’s actually three main types, and each one serves different purposes.

Treasury Bills (T-bills) mature in under a year, making them the safest bond option due to their short tenure – similar to a Certificate of Deposit but backed by the government. However, interest rate risk cuts the other way: if you buy a 6-month T-bill at 5% and rates drop to 3% when it matures, your next T-bill purchase will lock you into that lower 3% rate, reducing your future income stream. Despite this risk, sophisticated investors like Warren Buffett often park substantial cash in T-bills when attractive stock market opportunities are scarce, preferring the safety and liquidity over uncertain equity returns.

Treasury Notes (T-notes) occupy the middle ground with 2 to 10-year maturities and serve as crucial economic indicators. Investors use both 5-year and 10-year yields to gauge the country’s economic conditions, with each reflecting the risk associated with their respective time horizons – the 5-year captures medium-term economic uncertainty while the 10-year reflects longer-term risks and expectations. Together, these yields help investors assess overall economic health and future outlook. If I were limited to buying individual bonds for fixed income exposure, I’d focus on this intermediate range to balance interest rate risk while avoiding the decades-long commitment that ties your capital to the country’s long-term prospects.

Treasury Bonds (T-bonds) represent the marathon investment, extending 20 to 30 years into the future. While I’d never invest in these directly, I constantly monitor their yields as they serve as the benchmark for mortgage rates – when the 30-year Treasury yield rises from 3% to 4%, you can expect 30-year mortgage rates to climb from around 6% to 7%, directly impacting housing affordability and refinancing decisions. This connection explains why major news outlets like CNBC and The Wall Street Journal regularly report on 30-year Treasury yields and emphasize their importance – they’re tracking a key indicator that affects millions of homeowners and potential homebuyers.

Why Treasury Bonds Matter to Everyone

Treasury securities function as the foundation for interest rates across the entire financial system. When T-bond yields rise, mortgage rates climb in lockstep, credit card companies adjust their rates upward, demonstrating how these government securities ripple through every corner of consumer finance.

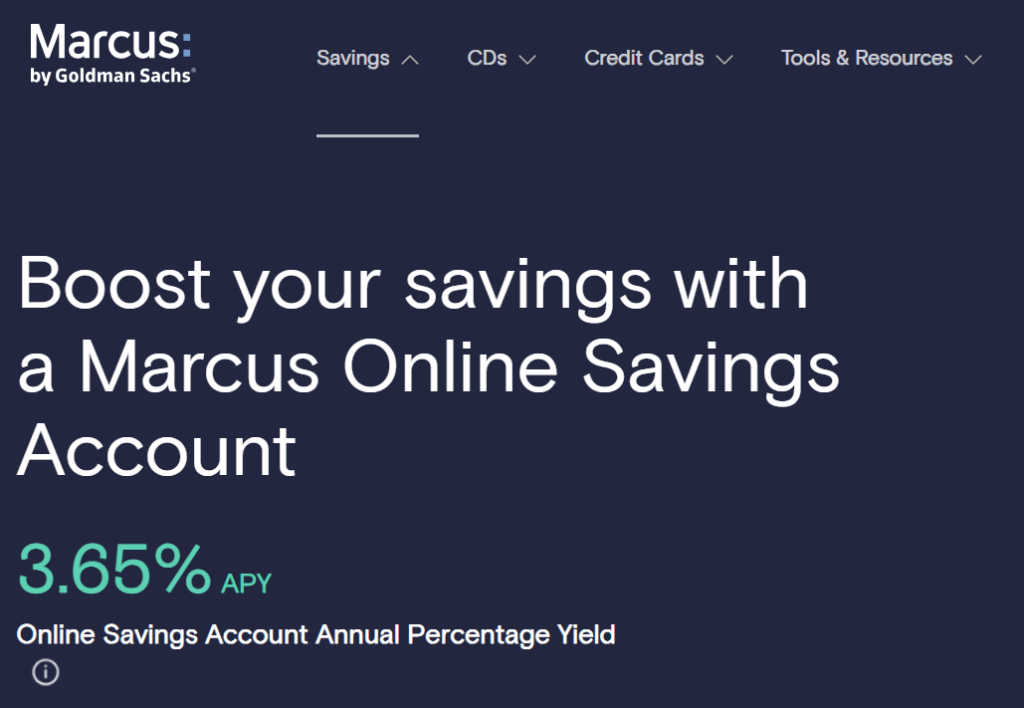

I experienced this rate connection firsthand when the Federal Reserve began lowering the benchmark federal funds rate in September 2024 – my Marcus savings account rates dropped precipitously from 5% to 3.65% over the following months, showing how quickly Treasury rate changes flow through to consumer products. While this hurt my savings yield, it reminded me that Treasury bonds and consumer rates move in tandem, creating opportunities in one area while reducing returns in another.

Treasury bonds serve as the financial system’s ultimate safe haven during market chaos. The 2020 market crash illustrated this perfectly: while stocks plummeted in violent swings, Treasury bonds maintained relative stability as investors executed the classic “flight to quality” – abandoning risky assets for the security of government-backed securities. This pattern repeats during every major crisis – whether the 2008 Financial Crisis or the pandemic, investors consistently dump stocks while flocking to Treasuries, reinforcing their role as the go-to refuge when markets turn volatile.

The “Risk-Free” Label (And What It Really Means)

Financial textbooks love calling Treasury bonds “risk-free,” but that term needs some unpacking. They’re risk-free in the sense that you’ll get your principal back at maturity, assuming the U.S. government doesn’t collapse. The default risk is essentially zero.

However, there’s still interest rate risk and inflation risk to consider. When I saw the yield on 10-year bond hovering at around 3%, I felt it is good investment. Then inflation started creeping up, and suddenly that fixed return wasn’t looking so attractive anymore.

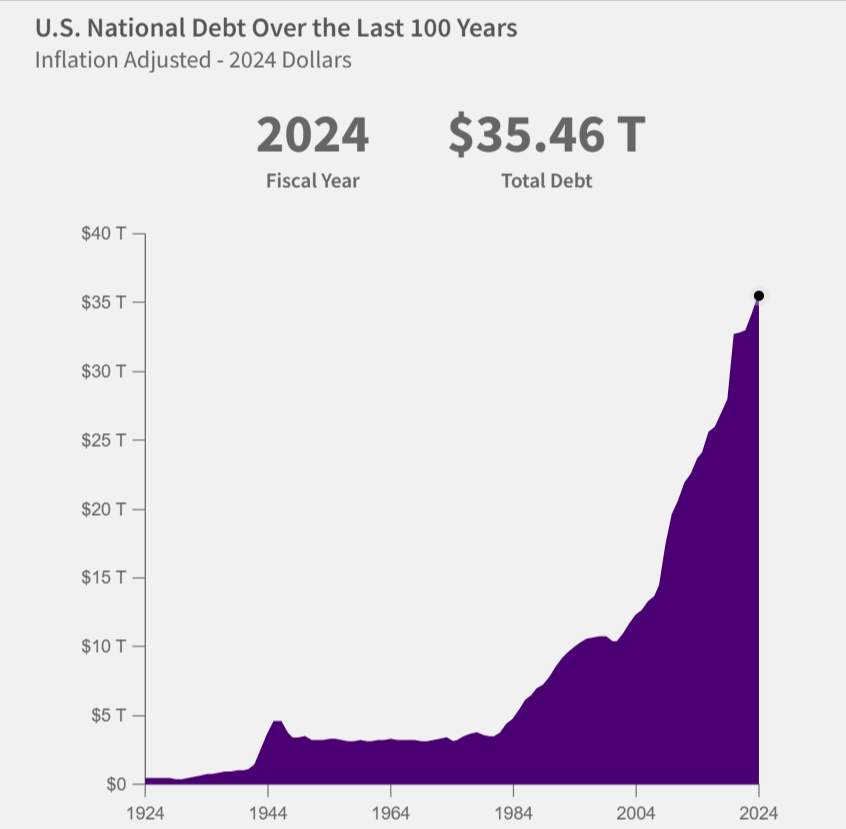

The current ballooning debt level adds another layer of concern that most investors overlook. With national debt spiraling upward without meaningful remedies, we’re likely setting ourselves up for a painful reckoning through either significant inflation as the government prints money to service obligations, or crushing tax increases to fund repayments. The Congressional Budget Office projects the federal budget deficit at $1.9 trillion in 2025, with federal debt rising to 118 percent of GDP by 2035, while Moody’s recent credit downgrade signals that debt is projected to reach 156 percent of GDP by 2055. Either scenario undermines the real value of Treasury returns, making today’s “risk-free” bonds potentially costly mistakes for long-term investors.

Picture from fiscaldata.treasury.gov

Tax Considerations That Actually Matter

Treasury bond interest enjoys federal taxation but remains exempt from state and local taxes – a significant advantage for residents of high-tax states like California or New York. Consider a practical example with a $10,000 investment in a 10-year Treasury note yielding 4.2% while living in California:

- Annual interest earned: $420

- Federal taxes owed: Based on your federal tax bracket

- California state taxes saved: ~$56 annually (13.3% top state rate avoided)

- Total benefit: Meaningful tax savings that compound over the 10-year holding period compared to taxable corporate bonds

This state tax exemption becomes increasingly valuable as both your income level and state tax rates rise.

The timing of tax payments varies depending on the type of Treasury security you own. With T-bills, you pay taxes on the discount when the bill matures. For notes and bonds, you’ll owe taxes on interest payments as you receive them each year.

Early in my Treasury investing, I overlooked tax efficiency by holding these securities in taxable accounts rather than maximizing their tax advantages. However, the optimal placement strategy depends on your liquidity needs: IRAs lock your money away until retirement with a 10% early withdrawal penalty before age 59½. For high-tax state residents, keeping Treasuries in taxable accounts provides a dual benefit – you capture the state tax exemption while maintaining full access to your funds without penalties. This liquidity advantage becomes especially valuable during emergencies when you need cash quickly, while other fully-taxable bonds might be better suited for tax-advantaged accounts where you can sacrifice immediate access for maximum tax shelter.

Treasury bonds might not be the most exciting investment you’ll ever make, but they serve an important role in building a solid financial foundation. Just don’t expect them to make you rich overnight – that’s not what they’re designed for.

Understanding Corporate Bonds (Private Sector Debt Securities)

Man, my first encounter with corporate bonds was a total disaster. I was scrolling through my brokerage account feeling pretty confident after dabbling in Treasury bonds, and I spotted some Ford Motor Company bonds yielding 6%. Compared to the measly 2.5% I was getting from government bonds, this looked like easy money.

Spoiler alert: it wasn’t that simple.

What Corporate Bonds Actually Are

Corporate bonds are basically companies asking to borrow your money, just like when your buddy asks for a loan to fix his car. Except instead of your buddy, it’s Microsoft or General Electric making the promise to pay you back with interest. The company gets the cash they need for expansion, new equipment, or debt refinancing, and you get regular interest payments plus your principal back at maturity.

The fundamental difference between corporate and government bonds hit me pretty quickly. When Uncle Sam issues a Treasury bond, there’s virtually no chance he won’t pay you back. When Sears issues a bond… well, we all know how that story ended. Companies can and do go bankrupt, which makes corporate bonds inherently riskier than their government counterparts.

What makes corporate bonds appealing is that extra yield you get for taking on that additional risk. It’s called the credit spread – the difference between what a corporate bond pays versus a comparable Treasury bond. That spread compensates you for the possibility that the company might run into financial trouble.

How Companies Use These Bonds to Raise Capital

I used to think companies only issued stock when they needed money, but corporate bonds are actually a huge part of how businesses finance their operations. Instead of giving up ownership stakes by issuing more shares, companies can borrow money through bond issuances and maintain control.

Take Apple, for example. They’ve got billions in cash overseas, but rather than paying hefty repatriation taxes, they’ve issued corporate bonds to fund operations in the U.S. It’s cheaper for them to borrow money at low interest rates than to bring their offshore cash home. Pretty clever, actually.

The bond market gives companies access to longer-term funding than bank loans typically provide. While a bank might loan money for 5-7 years, corporate bonds can stretch out 10, 20, or even 30 years. This lets companies plan major projects without worrying about refinancing every few years.

The Corporate Bond Spectrum

Here’s where I really messed up initially – I thought all corporate bonds were basically the same risk level. Wrong, wrong, wrong.

Investment-grade bonds come from companies with solid credit ratings, typically rated BBB- or higher by Standard & Poor’s. These are your blue-chip companies like Johnson & Johnson or Coca-Cola. The yields aren’t spectacular, but you can generally sleep well at night holding them.

Toyota: A+ (S&P & Fitch); A1 (Moody’s)

High-yield bonds, also known as junk bonds (though that term sounds harsher than it needs to), come from companies with credit ratings below investment grade. These bonds offer higher yields to compensate for increased default risk. When I saw the yield on Nissan, a famous Japanese carmaker, touching 7%, I was so excited to buy it until I started researching the company’s declining sales trends.

Nissan: BB (S&P); BB+ (Fitch); Ba1 (Moody’s

Convertible bonds are the weird hybrid creatures of the bond world. They give you the option to convert your bond into company stock at a predetermined price. I bought some convertible bonds from a tech company thinking I was being clever, but the conversion features made the pricing way more complicated than I anticipated.

Credit Ratings: The Report Cards That Matter

Understanding credit rating systems was like learning a new language for me. Moody’s, Standard & Poor’s, and Fitch are the big three agencies that grade corporate bonds like teachers grading homework.

Microsoft and J&J are the only companies with AAA ratings as of June 2025

The rating scale goes from AAA (practically bulletproof) down to D (default). Investment-grade ratings run from AAA down to BBB-, while anything below that falls into high-yield territory. I learned to pay attention to rating trends too – a company on “credit watch negative” might be heading for a downgrade.

Here’s something that caught me off guard: rating agencies don’t always agree. I used to believe that rating agency analysis was indisputable since they have all the tools to assess public companies. This made me think that any high ratings they assigned would indicate a safe investment.

The financial crisis taught everyone that rating agencies aren’t infallible. Those mortgage-backed securities that blew up in 2008 had been rated AAA right up until they weren’t. It’s a reminder that credit ratings are opinions, not guarantees.

| Investment grade | Moody’s | Standard & Poor’s | Fitch |

| Strongest | Aaa | AAA | AAA |

| Aa1 | AA+ | AA+ | |

| Aa2 | AA | AA | |

| Aa3 | AA- | AA- | |

| A1 | A+ | A+ | |

| A2 | A | A | |

| A3 | A- | A- | |

| Baa1 | BBB+ | BBB+ | |

| Baa2 | BBB | BBB | |

| Baa3 | BBB- | BBB- |

| Non-investment-grade | Moody’s | Standard & Poor’s | Fitch |

| Ba1 | BB+ | BB+ | |

| Ba2 | BB | BB | |

| Ba3 | BB- | BB- | |

| B1 | B+ | B+ | |

| B2 | B | B | |

| B3 | B- | B- | |

| Caa1 | CCC+ | CCC+ | |

| Caa2 | CCC | CCC | |

| Caa3 | CCC- | CCC- | |

| Ca | CC | CC |

| Weakest | Moody’s | Standard & Poor’s | Fitch |

| C | C | C | |

| D | D |

Industries That Love Issuing Bonds

Some sectors are absolutely bond-crazy, while others barely touch the corporate bond market. Utilities are huge bond issuers because they need massive amounts of capital for power plants and infrastructure projects. Their regulated business models make them relatively predictable, which bond investors appreciate.

Telecommunications companies are another big player in the corporate bond space. Building out cell tower networks and fiber optic cables requires enormous upfront investments that are perfect for bond financing. Bonds from Verizon and AT&T are almost utility-like in their stability.

Financial companies – banks, insurance companies, investment firms – are massive bond issuers, though their bonds can be trickier to analyze. Bank bonds were particularly volatile during the 2008 crisis, but they have been stable after the introduction of strict capital rules

Energy companies issue tons of bonds, but they can be boom-or-bust depending on commodity prices. I’ve read about cases where investors held bonds from oil companies that got crushed when crude prices collapsed. The high yields look attractive until the business fundamentals deteriorate.

Market Size and Getting Your Money Out

The corporate bond market is absolutely massive – we’re talking about $10 trillion in outstanding debt just in the U.S. But here’s the thing that surprised me: unlike stocks, most corporate bonds don’t trade on exchanges. They trade over-the-counter through dealer networks, which can make pricing less transparent.

Liquidity varies dramatically depending on the bond. Large, recent issues from well-known companies trade fairly easily, while smaller or older bonds can be tough to sell without taking a haircut on price. For this reason, it is sometimes difficult to buy and sell these bonds like day traders.

The corporate bond market tends to be less liquid than the stock market, especially for individual bonds. Bond ETFs and mutual funds have helped improve access, but if you want to own individual corporate bonds, be prepared for the possibility that selling might not be as straightforward as clicking a button.

Default Risk: The Elephant in the Room

Let’s talk about the scary stuff – what happens when companies can’t pay their debts. Historical default rates for investment-grade corporate bonds are actually pretty low, typically less than 0.5% annually. High-yield bonds default at much higher rates, sometimes reaching 10% or more during recession years.

Bondholders typically get paid before stockholders in bankruptcy proceedings, but recovery rates vary wildly depending on the company’s assets and the type of bond you hold.

Diversification becomes crucial when dealing with default risk. Holding bonds from 20 different companies across various industries reduces the impact if one or two companies run into trouble. It’s basic risk management, but it took me a few painful lessons to really internalize this concept.

Corporate bonds aren’t nearly as boring as I initially thought. They’re complex instruments that require homework and attention, but they can play an important role in a balanced portfolio when you understand what you’re getting into.

Key Differences Between Government and Corporate Bonds

The biggest difference between government and corporate bonds comes down to who’s backing your investment. Government bonds, especially U.S. Treasuries, are backed by the full faith and credit of the federal government – which basically means they have the power to print money or raise taxes to pay you back. Corporate bonds, on the other hand, are only as good as the company issuing them. When companies like Lehman Brothers or Enron went under, their bondholders learned this lesson the hard way. That fundamental difference in backing creates a huge gap in default risk between the two types of bonds.

The yield difference between the two really tells the story of risk versus reward. Corporate bonds typically offer higher interest rates to compensate investors for taking on credit risk – the possibility that the company might default. You might find corporate bonds yielding 5-6% when Treasuries are only paying 2-3%, but that extra yield isn’t free money. It’s compensation for accepting the possibility that things could go sideways with the issuing company. During economic downturns, this risk premium becomes very real as some corporate issuers struggle to meet their obligations.

Liquidity and tax treatment also separate these two bond categories significantly. Treasury bonds trade in one of the world’s most liquid markets – you can buy or sell them easily without much impact on price. Corporate bonds, especially smaller issues, can be much trickier to trade and often have wider bid-ask spreads. From a tax perspective, Treasury interest is exempt from state and local taxes, while corporate bond interest gets hit with the full tax treatment. If you live in a high-tax state like California or New York, this difference can actually add up to meaningful savings over time.

Conclusion

Choosing between corporate bonds and treasury bonds doesn’t have to be an either-or decision. Smart investors often include both in their portfolios to balance safety with higher returns!

Treasury bonds offer unmatched security and tax advantages, making them perfect for conservative investors or those nearing retirement. Corporate bonds, while carrying more risk, provide higher yields that can boost your overall portfolio returns. The key is finding the right mix that matches your risk tolerance and investment timeline.

Remember, successful bond investing isn’t just about picking the right type – it’s about understanding how these securities fit into your broader financial strategy. Consider starting with a small allocation to each type, monitor their performance, and adjust based on your comfort level and market conditions.