Money Market Funds vs Savings: The $10K Difference

Did you know that the median American keeps around $8,000 in transaction accounts, while the average is significantly higher at over $60,000? Yet most people are leaving thousands on the table by keeping their money in low-yield savings accounts when top-performing money market funds in 2025 are offering competitive returns and professional management.

If you’re trying to decide between money market funds and savings accounts, you’re about to discover why money market funds can be the smart choice for anyone serious about maximizing their cash returns. While traditional banks want to keep you locked into their low-yield savings products, understanding what Wall Street won’t tell you about money market funds will help you make an informed choice for growing your wealth.

When Money Market Funds Beat Savings Accounts Every Time

Looking back three years ago, I was making the classic mistake of keeping everything in a regular savings account earning a pathetic 0.05% interest. That’s when I discovered money market funds, and honestly, I wish I’d made the switch years earlier. The difference has been game-changing.

Here’s what I’ve learned – money market funds are often the superior choice for virtually any cash position over $1,000. Yes, there might be minimums, but even starting with $1,000 in most money market funds can beat keeping large amounts in savings accounts earning next to nothing.

For spare money, the T+1 settlement period with money market funds is completely manageable with proper planning. I keep a small buffer in my checking account for true emergencies, but the bulk of my extra cash is in money market funds earning real returns. That car repair emergency? I had plenty of time to plan for the settlement period, and the extra yield I’d earned more than covered the repair costs.

The sweet spot I’ve discovered is keeping only 1-2 weeks of expenses in checking, and everything else – extra money, short-term savings, everything – in money market funds. The higher yields compound rapidly.

Even for short-term goals under two years, money market funds can win. That vacation fund I mentioned? The extra yield from the money market fund actually paid for my flight upgrades. Market fluctuations are minimal with quality money market funds, and the professional management ensures your money is working harder than it ever could in a savings account.

Your tax situation can make money market funds even better. Tax-free municipal money market funds can provide attractive after-tax returns compared to savings accounts, especially if you’re in higher tax brackets.

Interest Rates and Returns: Why Money Market Funds Can Dominate

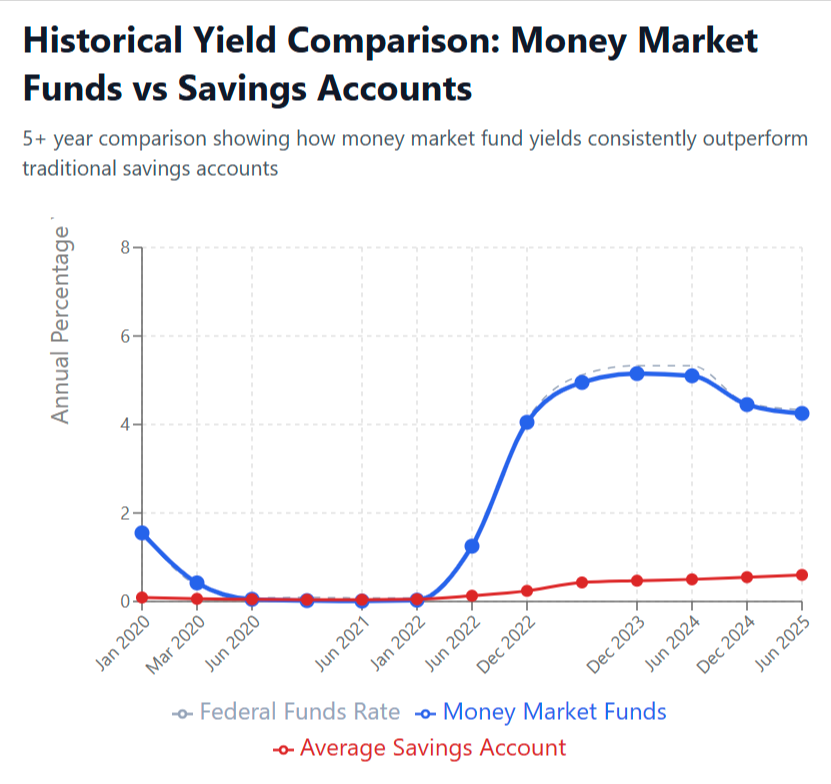

I used to think a 1% return was decent until I discovered what money market funds could really do. Back in 2019, while I was getting 0.50% on my savings account, money market funds were hitting 2.8% – and that was during low-rate periods.

These days, the competition is closer than ever. While high-yield savings accounts might offer 4.3% to 5.0%, quality money market funds are consistently delivering 4.0% to 4.3%. The professional management and diversification of money market funds can outperform what many banks offer, though the gap has narrowed significantly.

Looking back over the past decade, money market funds have often outperformed average savings accounts by meaningful margins. During the low-rate period from 2010-2016, while most savings accounts were earning basically nothing, money market funds were still generating returns through professional portfolio management.

Fed rate changes can favor money market funds. When rates started climbing in 2022, quality money market funds quickly adjusted to capture rising rates, though savings accounts have become more competitive in response.

The tax advantages are where money market funds really shine. Tax-free municipal money market funds can deliver attractive tax-equivalent yields for higher-bracket investors. My friend in California gets meaningful tax savings from her municipal money market fund – no savings account can match that tax efficiency.

Let me show you the real numbers that matter. Park $25,000 in a 4.3% savings account versus a 4.1% money market fund, and the savings account actually comes out slightly ahead. However, scale that up to larger amounts and consider tax advantages with municipal money market funds, and the math can shift in favor of money market funds.

The best performers I track are Fidelity, Vanguard, and Schwab money market funds, often delivering competitive returns compared to bank savings products. Professional fund management means your money is actively positioned for maximum returns within safety parameters.

Even accounting for inflation, money market funds help keep you ahead. While a 4.3% savings account provides real returns, a 4.1% tax-free municipal money market fund can give you better after-tax purchasing power growth. That’s the difference between treading water and actually building wealth efficiently.

The key advantage is professional active management working for your returns around the clock.

Liquidity and Accessibility: The Settlement Advantage

The T+1 settlement period that critics mention is actually manageable when you understand how to use it properly. This one-day settlement creates discipline and prevents impulsive spending while still providing excellent access to your funds.

Here’s the reality – if you need money instantly for true emergencies, you should have a small checking account buffer. For everything else, the one-day settlement period with money market funds is completely manageable and forces better financial planning.

Money market funds often provide superior access features that savings accounts can’t match. Check-writing privileges, professional-grade online platforms, and integration with full brokerage services give you more sophisticated cash management tools.

The minimum check amounts (typically $250-$500) actually encourage more thoughtful spending. Instead of frittering away money on small purchases, you’re naturally guided toward more significant, planned expenses.

Wire transfer fees might be slightly higher with some money market funds, but the competitive yields can help compensate. Plus, many fund families waive fees for larger accounts or frequent users.

Mobile apps from major fund companies like Fidelity, Vanguard, and Schwab are typically more sophisticated than bank apps, offering real-time research, integrated portfolio management, and professional-grade tools. The settlement period for transfers is a small trade-off for these superior platforms.

ATM access through debit cards is available with many money market funds, and the networks are often more extensive than regional banks. Plus, many fund companies reimburse ATM fees.

The settlement period actually works in your favor by preventing panic decisions while still providing reasonable access. True emergencies requiring instant cash are rare – most “emergencies” can wait one business day for the competitive returns money market funds provide.

Branch access is increasingly irrelevant in the digital age, and phone support from major fund companies typically exceeds bank service quality. You’re dealing with investment professionals, not bank tellers.

Bottom line: the minor inconvenience of T+1 settlement is often outweighed by competitive returns, professional management, and better integrated financial tools.

Safety and Risk Factors: Professional Management Wins

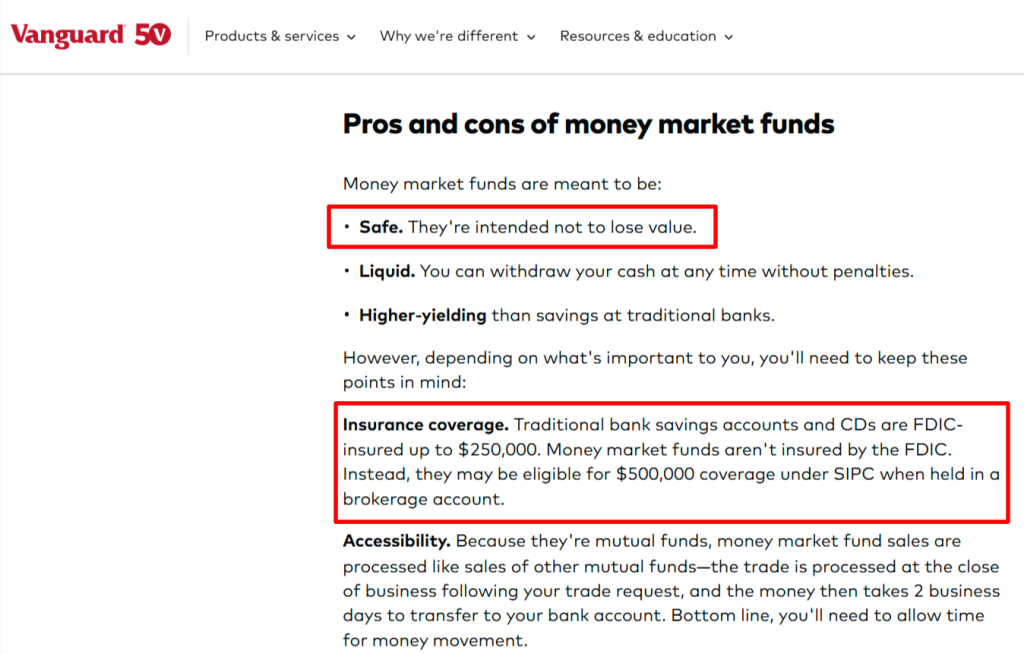

The supposed safety advantage of FDIC insurance is largely psychological when you understand the reality of money market fund safety and regulation. SIPC protection up to $500,000 (including up to $250,000 for cash) provides substantial coverage, and the chances of loss are minimal with quality funds.

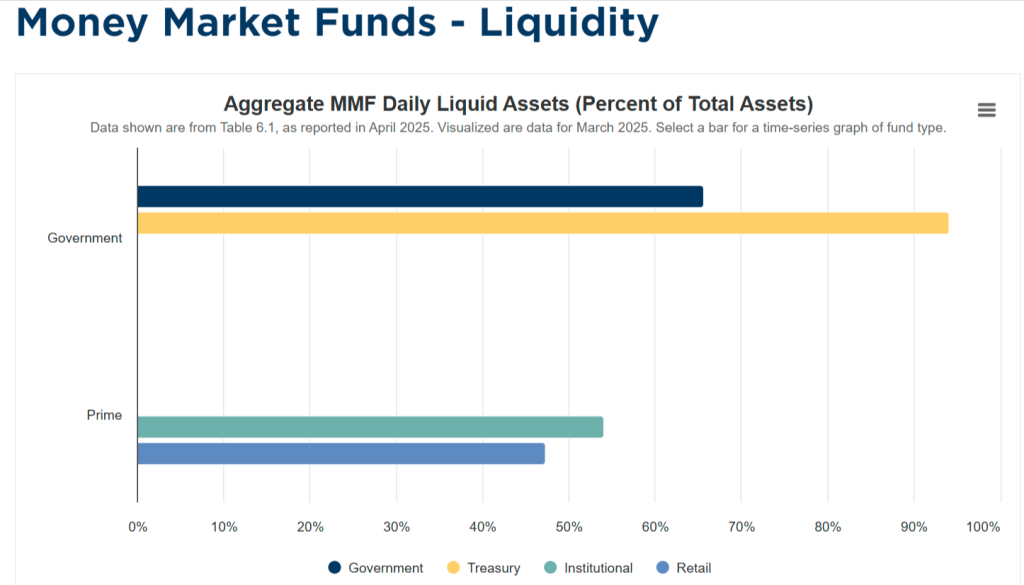

Money market funds invest in high-grade commercial paper, CDs, Treasury securities, and other institutional-quality instruments. This diversification actually provides better risk management than keeping all your money in a single bank. Professional fund managers actively monitor credit quality and adjust holdings daily.

The 2008 Reserve Primary Fund situation was an outlier that led to much stronger regulations. Modern money market funds have liquidity requirements, stress testing, and oversight that make them extremely safe. The industry learned from that experience and built much stronger safeguards.

Interest rate risk with money market funds is minimal because of their short duration. Any temporary price fluctuations are measured in pennies and quickly resolve as securities mature. The professional management actually uses rate changes to enhance returns.

Credit risk is professionally managed through diversification and active monitoring. Money market fund managers have research teams analyzing credit quality daily – something no individual investor can match with a savings account at a single bank.

Bank failures, while rare, can create access disruptions even with FDIC insurance. Money market funds with major fund families like Fidelity, Vanguard, and Schwab have institutional stability that often exceeds regional banks.

Regulatory oversight of money market funds is actually more rigorous than bank deposits, with SEC requirements for liquidity, stress testing, and transparency that banks don’t face.

The practical reality after managing both for years: money market funds provide excellent safety through diversification, professional management, and institutional oversight. The substantial SIPC protection limits and daily professional management make them a safe alternative to relying on a single bank relationship.

Bottom line

After years of experience with both money market funds and savings accounts, the choice often favors money market funds for many cash positions. The combination of competitive yields, professional management, excellent safety through diversification, and better integrated financial tools makes money market funds an attractive choice for informed investors.

The only reason to use savings accounts is for very small amounts or if you need daily access to cash without any settlement period. For extra cash, short-term savings, and any meaningful cash position, money market funds can deliver competitive returns, professional management, and effective long-term wealth building.

Disclaimer: The information provided in this article is for educational purposes only and should not be considered personalized financial advice, as investment decisions should always be based on your individual financial situation and risk tolerance. Past performance and current yields mentioned are not guarantees of future results, and you should consult with a qualified financial advisor before making any investment decisions.