Business to Consumer Payments: Old vs New Still Dominate

Did you know that 67% of consumers will abandon their purchase if their preferred payment method isn’t available? That’s a staggering statistic that highlights just how critical your payment strategy is to business success! Of course, your payment processing success also depends on having the right banking foundation and transfer capabilities in place – which is why understanding the best personal banking options and reliable wire transfer services can significantly impact your overall payment ecosystem performance.

In today’s rapidly evolving digital landscape, choosing the right business to consumer payment solutions can make or break your customer experience. Whether you’re a startup launching your first product or an established enterprise looking to optimize conversions, this comprehensive guide will walk you through everything you need to know about B2C payments in 2025.

Why I See These Payment Methods from the Inside

After 12 years as a corporate banker at one of the nation’s largest financial institutions, I’ve watched businesses make costly mistakes with their payment strategies every single day. Just last month, I had a client who was hemorrhaging money on transaction fees because they didn’t understand the difference between push to card and ACH transfers.

The wake-up call for me as a banker came when I realized how many business owners were flying blind with payment methods. I’d see companies paying thousands in unnecessary fees, or worse, losing customers because they only offered one or two payment options. That’s when I started diving deep into the mechanics of each payment rail and really understanding what works best for different business scenarios.

Push to Card: The Speed Demon

From my banker’s perspective, push to card is like the sports car of payment methods – fast, flashy, and you pay a premium for that performance. I recommend this to clients when they need to get money to someone’s debit card in minutes, not days. It works 24/7, which means your customers can get their refunds or payments even at 2 AM on a Sunday when traditional banking is closed.

Here’s what I tell my clients about the cost structure – and yes, you’re the one paying the fee while the recipient gets the full amount:

- Push to card: $1-3 per transaction

- ACH transfers: Often free or under $1 (but takes days)

- Wire transfers: $15-30

- Checks: Just postage (but seriously, it’s 2025)

What I love about push to card from a banking perspective is the reduced friction. Your customers don’t need to hand over their full banking details – just their debit card information, the same stuff they’d use for any online purchase. No routing numbers, no account numbers, no awkward conversations about what type of account they have.

But here’s the banker’s truth: when speed matters more than cost, push to card is worth every penny. I’ve seen too many businesses lose customers because they were “taking forever” with standard bank transfers.

Most of our push to card systems cap individual transactions at around $2,500 for person-to-person transfers, though business accounts can often go up to $10,000. For verified business disbursements, we can sometimes approve limits up to $50,000 or even $125,000 depending on your banking relationship and transaction history.

My rule of thumb for clients: push to card is perfect for anything under $500 where speed matters more than fees. Anything bigger, and we need to talk about your other options.

Push to Wallet: The Digital Native’s Choice

As a banker who works with a lot of fintech companies, I’ve watched push to wallet transform how younger demographics expect to receive payments. Instead of sending money to a traditional bank account or debit card, you’re loading funds directly into digital wallets like Venmo, Cash App, or Apple Pay. And like push to card, these systems operate 24/7.

The fee structure is similar to push to card, and again, you’re covering the cost while the recipient gets the full amount:

- Push to wallet: $0-3 per transaction (depending on funding source)

- Standard bank transfers: Free but takes 1-3 days

- Instant wallet transfers: 0.5-1.75% (usually capped around $15-25)

- Credit card funding: 3% (though many wallets are phasing this out)

From a banking compliance perspective, what I appreciate about push to wallet is the privacy protection. You only need someone’s username, phone number, or email – no sensitive banking information changes hands. That’s why I recommend it for businesses working with gig economy workers or younger contractors who prioritize privacy.

The speed is genuinely impressive from a technical standpoint. Most wallet payments appear instantly, which makes push to wallet ideal for businesses that need to pay workers immediately after task completion. The transaction limits are generous too – verified users can typically send $10,000+ per week, though new users start with much lower limits for fraud protection.

The banking reality check? Not everyone uses digital wallets, especially older customers who prefer traditional banking methods. Plus, if your recipient isn’t already on your preferred platform, they need to sign up and verify their account before you can send payment – that’s an extra friction point in your payment process.

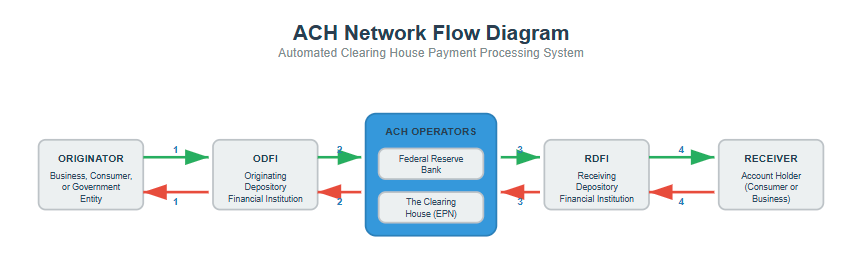

ACH: The Workhorse Everyone Should Use

ACH transfers are the backbone of modern business banking, and after 12 years in corporate banking, I can tell you they’re the most underutilized payment method out there. These electronic bank-to-bank transfers typically cost between $0.20-$1.50 per transaction, which is why I recommend them as the default payment method for most of my business clients.

Here’s the real cost breakdown I share with clients:

- ACH transfers: $0-$3 per transaction

- Wire transfers: $15-50 (painful for small amounts)

- Push to card/wallet: $1-3 per transaction

- Check processing: $0.50-2 (plus administrative overhead)

Some of our partner banks like Ally and Capital One don’t charge anything for ACH transfers, while traditional banks might charge $3-8 depending on speed options. At our institution, we offer same-day ACH, but there’s a 4:45 PM cutoff – miss that window and you’re waiting until the next business day.

The timing is where ACH requires some strategy. Standard ACH takes 1-3 business days to process, and they only work during banking hours. I always warn clients about Friday payments potentially not arriving until Tuesday because of weekends and banking holidays.

From a banking perspective, the privacy consideration is significant. Unlike digital wallets where you just need a username, ACH requires full banking details: routing numbers, account numbers, sometimes even a voided check. It’s more invasive than other payment methods, but it’s also more secure and regulated.

Here’s what makes ACH brilliant for businesses: batch processing capabilities and generous limits. Most of our business clients can process hundreds of payments simultaneously, and daily limits typically range from $10,000-$25,000 depending on your banking relationship. I’ve helped clients send payments to dozens of recipients for a total fee under $20.

My banker’s recommendation: ACH is perfect for regular, planned payments where you can work around the timing delays and recipients are comfortable sharing their full banking details.

Check Disbursements: Old School But Still Useful

I know, I know – as a banker in 2025, recommending checks feels like suggesting we go back to telegrams. But here’s the reality: some of my most sophisticated business clients still use check disbursements for specific situations. And with the federal government phasing out paper checks by September 2025, businesses are becoming the primary users of this payment method.

Check disbursement services through banking platforms are more competitive than most business owners realize:

- Check disbursement services: $1.25-$3.00 per check (including printing & mailing)

- DIY check printing: $4-20 per check (when you factor in security paper, postage, labor, and compliance)

- ACH transfers: $0-$3 per transaction

- Wire transfers: $15-50 per transaction

The timing is obviously the trade-off – we’re looking at 5-7 business days including mail delivery. But most of our check disbursement services offer same-day printing and mailing if you submit before their cutoff (usually between 11 AM-2 PM).

From my banking experience, I’ve learned who still prefers checks: construction companies (76% of our construction clients still use them), older contractors who don’t trust electronic payments, and businesses that need detailed paper trails for compliance auditing. Unlike digital wallets where you just need an email, checks require full banking details – but some clients actually prefer that level of formality and documentation.

The limits are generous since there’s no real-time processing constraint. You can batch hundreds of payments at once, and unlike electronic methods, there are no daily caps imposed by card networks or ACH processing limits.

My banker’s bottom line: match your payment method to your recipient’s preferences and your business timeline. Rush payment to a young freelancer? Push to wallet. Regular monthly payments to established contractors? ACH every time. Working with traditional businesses or need bulletproof audit trails? Sometimes a well-executed check disbursement is exactly what the situation calls for.

Understanding these four payment rails has helped me save my business clients hundreds of thousands in fees while improving their customer satisfaction scores. Trust me, knowing when to use each method is a game-changer for your cash flow management and customer relationships.

Conclusion

The payment landscape is evolving faster than ever, and businesses that don’t adapt risk losing customers to competitors who offer more flexible payment options. As we’ve seen throughout this guide, there’s no one-size-fits-all solution – the key is understanding your customer base and matching payment methods to their preferences and your business needs.

The data tells us that payment choice directly impacts your bottom line, with over two-thirds of consumers willing to abandon purchases when their preferred method isn’t available. By implementing a strategic mix of push to card for urgent payments, ACH for regular disbursements, digital wallets for younger demographics, and yes, even checks for traditional industries, you’re not just processing payments – you’re creating competitive advantage through superior customer experience.