Corporate Bonds for Beginners: Why Most Fail (Avoid This) 2025

Did you know that the global corporate bond market is worth over $36 trillion? That’s a staggering amount of wealth-building potential sitting right at your fingertips! If you’re tired of watching your savings earn practically nothing in traditional bank accounts, corporate bond investing might be your ticket to generating steady income while preserving capital.

But here’s the thing – I’ve been working as a corporate banker for over a decade, and I see beginners get overwhelmed by the complexity of bond markets all the time, whether they’re choosing between the best corporate bond ETFs for 2025 or trying to find the right bond ETF brokers to get started. By the end of this guide, you’ll understand exactly how to start building a solid fixed-income portfolio that works for your financial goals, with all the complex terms like “yield to maturity,” “credit ratings,” and “duration risk” broken down in plain English.

Understanding Corporate Bond Risks and Credit Ratings

Look, I’ll be straight with you – I’ve watched too many clients learn about corporate bond risks the hard way. Just last year, I had a client who thought he was being smart by loading up on some “high-yield” corporate bonds without understanding what that really meant. Spoiler alert: high-yield often means high-risk, and boy did he find that out quick.

Credit Risk Hits Harder Than You Think

Credit risk is basically the chance that a company won’t pay you back, and man, I’ve seen it devastate portfolios faster than you’d believe. I had this client back in 2018 who invested heavily in what seemed like a solid retail company’s bonds paying 7.5% annually. Six months later, they filed for Chapter 11 bankruptcy. That’s when he realized that even established companies can default on their debt obligations faster than you’d think.

The thing about defaults is they don’t always mean you lose everything – sometimes bondholders get cents on the dollar through bankruptcy proceedings. But I’ve sat across from clients who waited two years to maybe get 30% of their money back. Those conversations are never fun.

Interest Rates Are Your Frenemy

Here’s something that trips up a lot of my clients: when interest rates go up, bond prices go down. It’s like a seesaw that never stops moving. I remember one client holding a 10-year corporate bond paying 4% when the Fed started raising rates aggressively in 2022. New bonds were suddenly offering 6%, making his worth way less if he needed to sell early.

The duration of your bond matters huge here. I always tell clients that longer-term bonds get hit harder by rate changes than shorter ones. A 20-year bond might drop 15-20% in value when rates jump just 1%, while a 2-year bond barely budges. I’ve seen this play out in client portfolios countless times.

Inflation Quietly Steals Your Lunch Money

Inflation risk is sneaky because it doesn’t show up in your account balance right away. You’re still getting your interest payments, but your purchasing power is getting eaten alive. I had clients holding bonds during 2021-2022 when inflation jumped to over 8% while their bonds were only paying 4.5%. Technically they were losing money every month, even though the statements looked fine (but better than sitting in your savings account and earning pennies).

Liquidity Can Be a Real Problem

Corporate bonds aren’t like stocks where you can hit “sell” and get your money in seconds. I’ve had clients learn this lesson the hard way. Some corporate bonds, especially smaller issuers or longer maturities, can take days or weeks to find buyers. Just last month, I had a client trying to sell a mid-sized utility company’s bonds, and it took three weeks just to get a decent bid. The spread between what buyers wanted to pay versus what sellers wanted was ridiculous.

Decoding Those Credit Ratings

Credit rating agencies like Moody’s, S&P, and Fitch are supposed to help you understand risk, but I spend half my time explaining their systems to confused clients. Here’s the breakdown that finally makes sense to most people:

Investment Grade (the “safe” stuff):

- AAA/Aaa: Government-level safety

- AA/Aa: Super solid companies like Microsoft

- A: Good companies with stable cash flows

- BBB/Baa: Decent but watch for downgrades

Junk Territory (higher risk, higher reward):

- BB/Ba and below: Here be dragons

The key thing I always stress to clients is that ratings can change, and when they do, bond prices move fast. A downgrade from BBB to BB means your “investment grade” bond just became junk, and I’ve seen prices drop 10-15% overnight when this happens.

Always check the outlook too – “negative” means a downgrade might be coming. Trust me, I’ve learned to pay attention to that stuff on behalf of my clients.

How to Buy Corporate Bonds: A Step-by-Step Guide

When clients first decide to buy corporate bonds, they often make the rookie mistake of thinking any old brokerage account will work just fine. I see this all the time, and I have to break the bad news that not all brokerages are created equal when it comes to bond investing.

Picking the Right Brokerage (This Matters More Than You Think)

You need a brokerage that actually has a solid bond platform. I’ve had clients start with popular commission-free brokers only to discover their bond selection was terrible – maybe 200 corporate bonds total. When they switch to bond brokers, suddenly they have access to thousands of bonds with way better research tools.

From my experience working with various platforms, look for brokers that offer comprehensive bond screeners, real-time pricing, and decent inventory. The research tools matter more than most people realize.

Primary vs. Secondary Market: Where the Action Really Happens

Here’s something that confuses my clients for months: there are basically two ways to buy corporate bonds. Primary market is when companies first issue new bonds – think of it like an IPO for bonds. Secondary market is where people trade bonds that already exist.

Most retail investors end up buying in the secondary market because that’s where the selection is. Primary market offerings usually require bigger minimum investments, like $100,000 or more. Unless you’re working with a wealth manager, you’ll probably be shopping the secondary market like everyone else.

Those Pesky Minimum Investment Requirements

Corporate bonds typically come in $1,000 increments, but here’s the catch I have to explain to clients – many brokers require minimum purchases of $5,000 or even $10,000 for individual corporate bonds. I see disappointment on clients’ faces when they try to buy just one $1,000 bond and get rejected.

Some brokers like Fidelity will let you buy single bonds for $1,000, but the selection gets limited. If you’ve got less than $25,000 to invest in bonds, I usually recommend considering bond funds or ETFs instead.

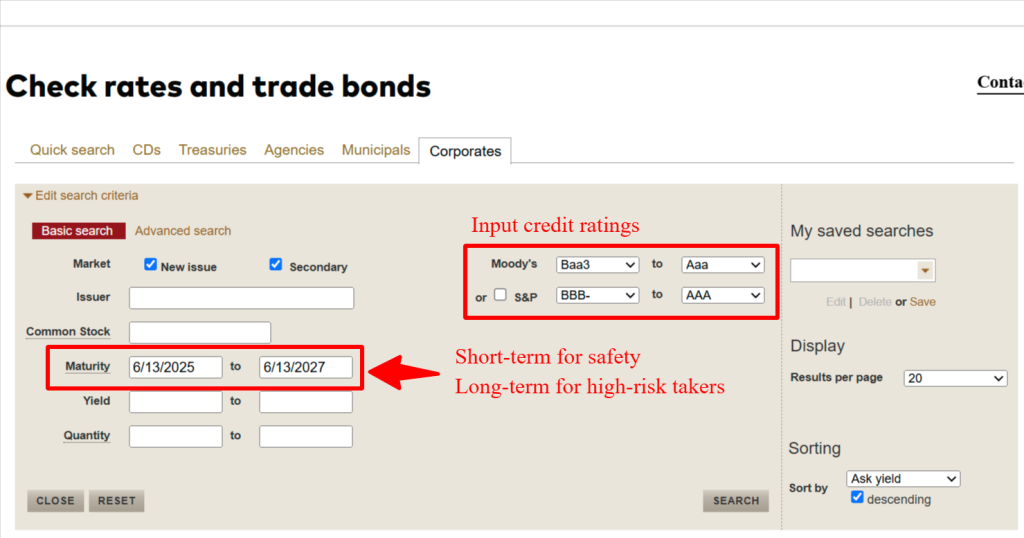

Bond Screeners Are Your Best Friend

Learning to use bond screeners properly takes most of my clients way longer than it should. Most platforms let you filter by credit rating, maturity date, yield, and sector. I usually teach clients to start by filtering for investment-grade bonds (BBB and above) with maturities between 3-10 years.

Pro tip from years of experience: always check the “callable” feature. Some bonds can be called back by the company before maturity, which totally screws up your plans. I’ve seen clients get burned on this with utility bonds that got called just two years in when rates dropped.

Bid-Ask Spreads Will Eat Your Lunch

This is where bond trading gets expensive fast, and I have to educate clients about this constantly. The bid-ask spread is the difference between what buyers want to pay and what sellers want to receive. On popular investment-grade bonds, spreads might be 0.25-0.50%. On smaller or junk-rated bonds, I’ve seen spreads as wide as 2-3%.

I always tell clients to check the spread before buying. If it’s wider than 1% on an investment-grade bond, you’re probably getting ripped off.

Individual Bonds vs. Funds: The Eternal Debate

This is probably the most common question I get from clients. Individual bonds give you control and predictable income if you hold to maturity. Bond funds give you diversification and liquidity but no maturity date guarantee. I usually recommend both – individual bonds for your “hold forever” money and bond ETFs for stuff you might need to sell.

For beginners with less than $50,000, honestly I just tell them to start with bond ETFs like AGG or LQD. Way less hassle, and you can always graduate to individual bonds later.

Common Mistakes to Avoid When Investing in Corporate Bonds

Oh man, where do I even start with corporate bond mistakes? I’ve watched clients make pretty much every dumb move in the book over my decade in banking, and let me tell you – some of these errors have cost them serious money. The good news is you can learn from their screw-ups without losing your own cash.

The Yield-Chasing Trap Almost Breaks Portfolios

Back in 2019, I had multiple clients asking about this energy company bond paying 9.5% while everything else was offering maybe 4-5%. Their greedy brains went “jackpot!” without bothering to ask why they were paying such crazy high interest. Six months later, oil prices tanked and those bonds dropped 40% in value.

Here’s what I’ve learned from watching this pattern repeat: when a bond yields way more than similar companies, there’s usually a damn good reason. High yield almost always means high risk. Those 8-10% corporate bond yields? They’re not free money – they’re danger pay.

Putting All Eggs in One Sector (Big Oops)

One of my biggest client disasters was when this guy loaded up on retail company bonds in early 2020. He figured people would always need clothes and stuff, right? Then COVID hit and retail got absolutely destroyed. Suddenly 60% of his bond portfolio was tied to companies that couldn’t even keep their stores open.

I learned to always stress that credit quality matters huge, but so does spreading your risk around. Now I never let clients put more than 15% of their bond money in any single sector. Energy, retail, airlines – these sectors can all get hammered at once if the wrong thing happens.

Terrible Timing With Interest Rates

In late 2021, I had several clients decide to buy bunches of 20-year corporate bonds because the yields looked decent. Problem was, everyone and their brother could see that the Fed was about to start raising rates aggressively. Within six months, their long-term bonds were down 25% because new bonds were offering way better rates.

The lesson here isn’t to time the market perfectly (impossible), but don’t ignore obvious rate trends. When rates are at historic lows and inflation is picking up, maybe don’t lock yourself into 30-year bonds. I try to help clients see these big picture trends.

Liquidity Bites When Clients Need Cash

I thought one client was being smart by buying bonds from smaller companies with better yields. What he didn’t realize was how hard it would be to sell them when he needed money for a house down payment. Some of those bonds took weeks to find buyers, and the bid-ask spreads were brutal – like 3-4% just to get out.

I always tell clients to keep some portion of their bond investments in highly liquid stuff like large company bonds or bond ETFs. You never know when life will throw you a curveball.

Call Provisions Ruin the Best-Laid Plans

This one really ticks off my clients. I had one buy utility bonds paying 6% when rates were higher, thinking he was set for the next 10 years. Two years later, rates dropped and the company called the bonds back early. Suddenly he’s stuck reinvesting at much lower rates.

I always check if bonds are callable before recommending them to clients. If they are, I assume they’ll get called if rates drop significantly. It’s like the company gets to have their cake and eat it too, while you get screwed on reinvestment.

The bottom line from years of watching client portfolios? Start small, diversify like crazy, and don’t get greedy. Bonds are supposed to be the boring part of your portfolio that pays steady income. Keep them boring, and they’ll serve you well.

Bottom Line

After walking hundreds of clients through their first corporate bond investments, I can tell you this much – the investors who succeed are the ones who start with the basics and build from there. Don’t try to be a hero chasing the highest yields or timing interest rate moves perfectly. Those strategies have a funny way of blowing up in your face when you least expect it.

The corporate bond market has grown into a massive $36 trillion opportunity, but that size means there’s room for both smart investors and people who’ll get their heads handed to them. Start with investment-grade bonds, diversify across sectors, and use bond funds if you’re working with smaller amounts – your future self will thank you for keeping it simple and avoiding the expensive mistakes I see every single day.