How ACH Payments Work: 3-Day Secret That Saves Millions

Did you know that over 29 billion ACH transactions were processed in 2024, totaling more than $76 trillion? If you’ve ever received direct deposit from your employer or paid a bill online, you’ve likely used ACH payments without even realizing it. Choosing the right banking platform for digital payments and personal banking services can significantly impact your ACH experience, from processing speeds to fees.

But what exactly are ACH payments, and how do they work behind the scenes? This comprehensive guide will break down the essential financial system that quietly powers much of our digital economy, whether you’re a business owner considering ACH for your company or simply curious about how your money moves electronically.

The ACH Payment Process: Step-by-Step Breakdown

Man, when I first started working at the bank back in 2022, ACH payments were this mysterious black box that somehow moved money around. I remember staring at transaction logs thinking “how the heck does my rent payment actually get from my account to my landlord’s?” It wasn’t until I started digging into the backend processes that I realized just how elegantly choreographed this whole dance really is.

How It All Begins: The Initiation Phase

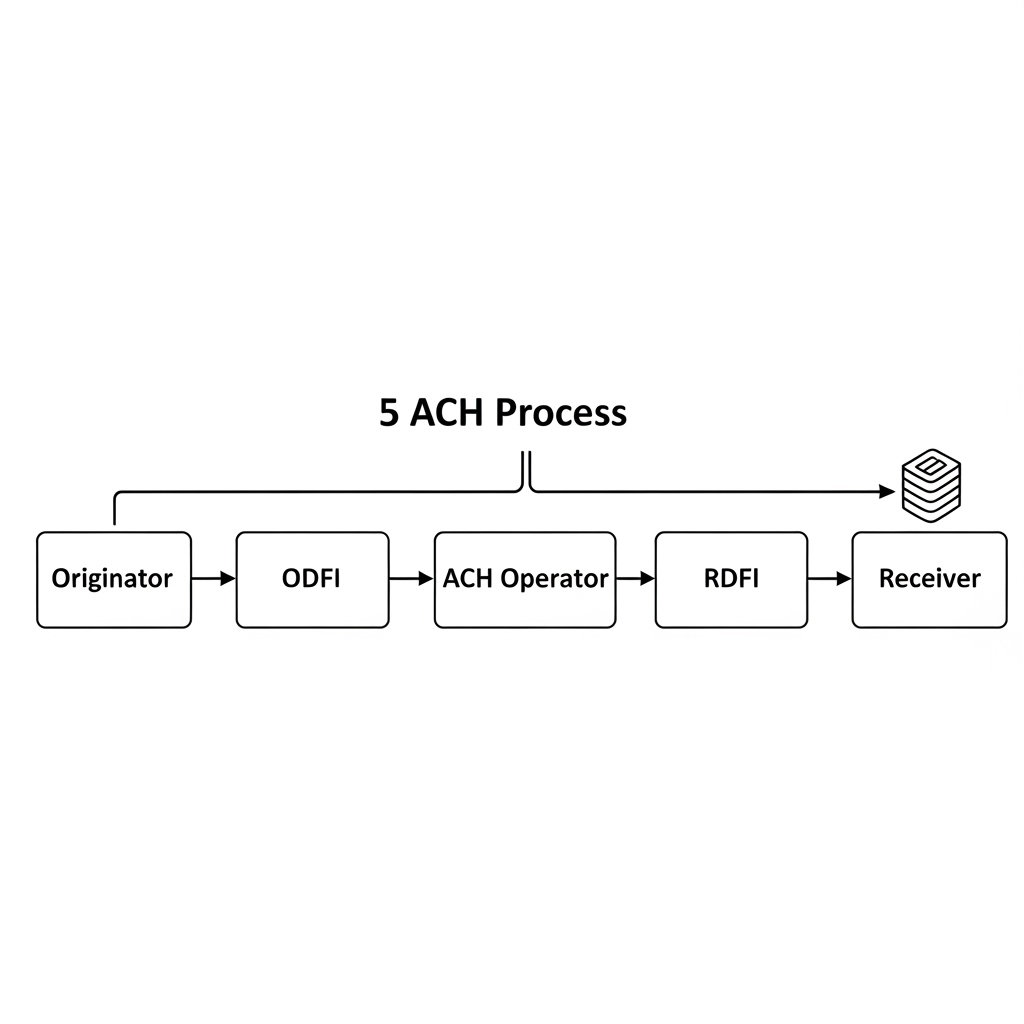

Every ACH transaction starts with what we call an “originator” – that’s fancy bank speak for whoever’s starting the payment. Could be you setting up autopay for your car loan, or your employer pushing payroll through the system.

Here’s where it gets interesting though. The originator doesn’t just hit send and hope for the best. They’ve gotta work through an ODFI (Originating Depository Financial Institution) – basically their bank (JPMorgan, Bank of America, Wells Fargo). I’ve seen so many clients get confused about this step because they think their payment goes directly to the recipient. Nope! Your bank is actually the middleman that packages everything up properly.

If you are a sender of money, your bank collects all the payment details: routing numbers, account numbers, transaction amounts, and those SEC codes that tell us what type of payment we’re dealing with. PPD for consumer payments, CCD for corporate stuff – there’s a whole alphabet soup of codes that took me months to memorize.

Batch Processing: The Daily Grind

This is where things get really cool. Unlike wire transfers that go through individually (and cost a fortune), ACH transactions get bundled together in batches. Think of it like a mail truck – instead of making individual trips for each letter, the postal service waits until they have a full load.

Banks typically submit these batches multiple times throughout the day. At our institution, we usually do three submission windows: morning, afternoon, and evening. I learned this the hard way when a client called panicking because their 4 PM payment didn’t hit the same day – turns out they’d missed our final cutoff at 3:30 PM.

The batch gets formatted into specific file types (usually NACHA format if you’re curious) and sent off to ACH operators. There’s tons of validation happening here too – account number check digits, routing number verification, all that good stuff that prevents money from going into the digital void.

The Federal Reserve and EPN: The Heavy Hitters

Once those batches leave the ODFI, they head to one of two main ACH operators: the Federal Reserve (FedACH) or the Electronic Payments Network (EPN). About 70% of ACH volume goes through the Fed, while EPN handles most of the rest.

These operators are basically the traffic controllers of the ACH network. They sort transactions by destination, run fraud checks, and route everything to the right receiving banks. The Fed processes ACH files four times a day during weekdays, which is why you’ll sometimes see same-day ACH options (though those cost extra).

What blew my mind when I first learned this was the sheer scale. We’re talking about processing over 25 billion ACH transactions annually worth more than $50 trillion. That’s a lot of rent payments and direct deposits flying around!

Why these two processors or “middle man” exist

You know, when I first started digging into ACH processing at work, I kept asking my supervisor “why the heck do we need these middlemen instead of just sending money directly between banks?” Turns out there’s actually some brilliant reasoning behind it. Back in the 1970s, the ACH system evolved from multiple regional clearinghouses – it was kind of a mess, honestly. The Federal Reserve jumped in to keep things stable, but the big banks weren’t gonna let the government control everything, so they created The Clearing House (which runs EPN) as their own private alternative. Smart move that created healthy competition.

The scale problem alone would make direct connections impossible. I did the math once during a slow afternoon – with over 10,000 banks and credit unions in the US, you’d need about 50 million individual connections if everyone connected directly to everyone else. Each connection would need its own agreements, technical standards, security protocols… my head started spinning just thinking about it. Plus, without ACH operators acting like universal translators, every bank would need to speak every other bank’s “language.” ACH operators eliminate all that nonsense by standardizing everything into NACHA format.

Settlement would be an absolute nightmare without intermediaries. When banks send money to each other, someone needs to actually move the real dollars between their Federal Reserve accounts. Without ACH operators, you’d have thousands of banks all trying to settle individually with thousands of other banks – the Fed would be drowning in settlement requests. ACH operators batch everything together and handle settlement in bulk, which is way more efficient. Plus, each direct connection would need its own risk assessment and fraud monitoring, but small banks don’t have resources to monitor patterns across thousands of institutions. ACH operators see the big picture and can spot fraud patterns that individual banks would miss.

Having two competing operators (Fed and EPN) actually keeps things interesting. I’ve seen this firsthand when we’re negotiating processing fees – banks can shop around and pit the Fed against EPN for better rates. It’s like having two grocery stores in town instead of just one. The Fed operates more like a public utility focused on stability, while EPN runs more like a business that needs to turn a profit. This creates different approaches to pricing, processing windows, customer service, and innovation timelines. Plus, if one system goes down (and yeah, it happens), the other can handle extra volume – crucial when you’re moving trillions of dollars around.

The whole setup reminds me of why we have airports instead of everyone flying point-to-point between every possible destination. Yeah, ACH operators take a small cut (pennies per transaction), but they eliminate massive costs like thousands of bilateral agreements, duplicate systems, and individual compliance monitoring. They create what economists call “network effects” – a tiny credit union in rural Montana can send money to Chase in New York just as easily as Chase can send to Bank of America. The ACH operators aren’t just middlemen taking a cut – they’re actually making the whole system work better and cheaper than it ever could with direct connections.

Settlement and Clearing: The Money Actually Moves

Here’s where the rubber meets the road, and honestly, this part confused me for months when I started. Settlement happens through the Federal Reserve’s account system – think of it like a massive spreadsheet where every bank in America has their own checking account with the Fed. When your ACH payment clears, real dollars actually move between these bank accounts at the Federal Reserve.

Remember how I mentioned earlier that transactions get bundled together like mail in a truck? Well, “batching” just means your individual payment gets grouped with thousands of others before getting sent out. Instead of processing your $500 rent payment by itself, your bank waits until they have a whole pile of payments, then sends them all at once. It’s way more efficient than handling each payment separately.

The timeline usually works like this:

- Day 1: Your payment gets initiated and thrown into the batch with everyone else’s

- Day 2: The batch gets processed by the ACH operator and delivered to your landlord’s bank

- Day 3: Money shows up in your landlord’s account (and disappears from yours)

But here’s the kicker – same-day ACH can compress this whole thing into just a few hours instead of days. It costs more (around $0.20 per transaction versus $0.03 for standard), but sometimes speed matters more than saving a few cents. I learned this when my own mortgage payment was running late and I didn’t want to get hit with fees!

Final Posting: When Money Becomes Real

The receiving bank (RDFI in our jargon) gets the ACH file and has to post transactions to customer accounts. This isn’t as simple as it sounds – they’re running their own validation checks, looking for account closures, insufficient funds, all sorts of potential roadblocks.

Most banks post ACH credits early in the morning, usually between 6-8 AM. Debits often get processed overnight. I always tell clients that just because they see pending transactions doesn’t mean the money has actually moved yet – that’s just the bank showing you what’s coming.

ACH Payments: The Good, The Bad, and The “Why Is This Taking So Long?”

When I first started using ACH for my own bills back in 2023, I was pretty much just thinking “free money transfers, sweet!” But after working with it professionally for a couple years now, I’ve learned there’s definitely some trade-offs you gotta consider. It’s not all sunshine and rainbows, though honestly, the benefits usually outweigh the headaches.

The Good Stuff: Why ACH Rocks

Cost-Effectiveness That’s Hard to Beat

- ACH transactions typically cost between $0.03 to $0.20 per transaction for standard processing

- Wire transfers can run you $15-50 each (I learned this the expensive way)

- Even same-day ACH at $0.20 is still way cheaper than wires

- Perfect for recurring payments like rent, utilities, loan payments

Reliability and Security

- Built-in fraud protection through the banking system

- Reversible if there are errors (unlike cash or some other payment methods)

- Established network that’s been running since the 1970s

- Banks are required to follow strict security protocols

Convenience for Recurring Stuff

- Set it and forget it for monthly bills

- No need to write checks or remember due dates

- Works great for payroll direct deposits

- Can handle both one-time and recurring transactions

The Not-So-Great Parts: Where ACH Falls Short

Speed Isn’t Its Strong Suit

- Standard ACH takes 1-3 business days (weekends don’t count)

- Same-day ACH exists but costs more and has cutoff times

- Can’t process on weekends or federal holidays

- If you need money moved RIGHT NOW, you’re out of luck

Transfer Limits Are Way Lower Than You’d Think

- While NACHA technically allows up to $1 million for same-day ACH, your bank probably caps you way lower

- Most banks limit you to $1,000-$25,000 per day

- Large transactions like buying a house or car often require multiple days of transfers or switching to wire transfers

Limited International Options

- ACH is basically a US-only system

- Can’t send money internationally through standard ACH

- International wires are your only option for overseas transfers

When ACH Makes Sense (And When It Doesn’t)

I always tell clients that ACH is perfect for the boring, predictable stuff – rent, utilities, loan payments, employee salaries. It’s cheap, reliable, and once you set it up, you can basically forget about it. But if you’re buying a house and need to move $50K for closing? You’re looking at multiple days of transfers even with the most generous bank limits, or you’ll need to pay for a wire transfer.

The sweet spot is really for amounts under $10K that don’t need to move immediately. I use ACH for pretty much all my personal bills now, but when I helped a client move $15K for a car purchase last year, even his $5K daily limit meant we had to plan it out over three days. Sometimes you just gotta bite the bullet and pay wire transfer fees for bigger amounts.

Bottom Line

Looking back at everything we’ve covered, ACH payments really are the financial world’s best-kept secret for saving money and staying secure. When I think about paying $0.03 for an ACH transfer versus $25 for a wire, or how my employer can process thousands of payroll payments for pennies each instead of hundreds in wire fees, the cost savings are just mind-blowing. Plus, the built-in fraud protection and reversibility that comes with the banking system gives me way more peace of mind than other payment methods – if something goes wrong, there’s actually a paper trail and process to fix it.

The reality is that for most businesses and individuals, ACH hits that sweet spot of being both dirt cheap and surprisingly secure. Sure, it’s not the fastest option out there, but when you’re moving money regularly – whether it’s paying bills, processing payroll, or collecting payments – those pennies per transaction add up to serious savings compared to alternatives. After working with this system for a few years now, I can confidently say that understanding ACH’s cost and security advantages has made me both a better banker and a smarter consumer.