Money Market Fund Stability Crisis: Are You Protected?

I’m always amazed that money market funds hold over $8 trillion in assets globally. I find it fascinating that they’ve become one of the most crucial components of our financial system. Yet, I’ve observed that during times of market stress, these seemingly stable investments can face unprecedented challenges that threaten the entire financial ecosystem.

In this comprehensive guide, I’ll walk you through the intricate world of money market fund stability mechanisms – from regulatory frameworks and liquidity buffers to redemption gates and NAV volatility controls. Whether you’re researching the the top money market funds for 2025or want to understand what Wall Street won’t tell you about these investments, I’ll give you the insights you need to navigate this complex landscape with confidence.

Money Market Fund Stability: Core Concepts and Importance

I’ll never forget the day I first heard about the Reserve Primary Fund breaking the buck back in 2008. It was during one of my training sessions when I started at the first bank in 2022, and our senior analyst was explaining why money market fund stability isn’t just some boring regulatory topic – it’s literally the foundation that keeps our entire short-term funding system from collapsing.

At first, I thought money market funds were just boring cash parking spots. The more I learned, the more I was wrong about its concept.

What Money Market Fund Stability Actually Means

Source from Vanguard

When we talk about stability mechanisms in money market funds, we’re really talking about the systems designed to keep these funds trading at exactly $1.00 per share. Sounds simple, right? It’s anything but simple when you dig into it.

The main stability mechanisms include:

- Amortized cost accounting – This lets funds value securities at their purchase price rather than market price, smoothing out daily fluctuations

- Sponsor support – Fund companies can step in with financial backing when things get rocky

- Liquidity requirements – Funds must hold certain percentages in daily and weekly liquid assets

- Stress testing – Regular analysis of how funds would perform under various market scenarios

I spent months researching these mechanisms for client presentations, and what struck me was how interconnected everything is. When one part breaks down, the whole system can unravel fast.

The 2008 Wake-Up Call That Changed Everything

The Reserve Primary Fund crisis was basically a perfect storm that nobody saw coming. When Lehman Brothers went under, this fund held $785 million in Lehman debt. That pushed their net asset value to $0.97 per share – breaking the sacred $1.00 barrier.

What happened next was pure chaos. Investors pulled out $60 billion in redemption requests from the $62 billion fund in just a few days. The entire commercial paper market nearly froze because companies couldn’t roll over their short-term debt.

Here’s what really gets me about this situation – it wasn’t just about one fund making bad investments. The whole system was built on this assumption that money market funds were basically risk-free. When that assumption cracked, panic spread like wildfire.

Who Really Depends on These Funds Working

After working with different types of clients, I’ve seen firsthand how many people rely on money market fund stability:

Individual Investors:

- Use these funds to park extra cash between investments

- Rely on the $1.00 share price for predictable account values

- Often don’t realize they’re taking on credit risk

Corporations:

- Need reliable short-term funding through commercial paper markets

- Use money market funds for cash management operations

- Depend on stable pricing for treasury operations

Financial Institutions:

- Rely on these funds as a funding source for loans and operations

- Use them for liquidity management

- Face serious problems when fund flows become unpredictable

I’ve had corporate clients tell me they never really thought about what happens if their money market fund “breaks the buck” until I walked them through the 2008 scenario. It was an eye-opener for both of us.

The Real Economic Impact

The difference between stable and unstable money market fund environments is huge. When these funds work properly, they provide about $4.5 trillion in short-term funding to the U.S. economy. When they don’t work, that funding can disappear almost overnight.

During my research, I found that unstable periods typically see:

- Commercial paper rates spike by 2-3 percentage points

- Corporate funding costs increase significantly

- Bank lending conditions tighten across all sectors

- Small businesses struggle to access working capital

The crazy part is how quickly things can change. One day everything’s fine, the next day companies can’t roll over their debt. That’s why regulators have spent so much time since 2008 trying to build better safety nets.

Understanding money market fund stability isn’t just academic – it’s about recognizing a critical piece of financial infrastructure that most people take for granted. The 2008 crisis showed us what happens when that infrastructure cracks, and honestly, we’re still working on making sure it doesn’t happen again.

Regulatory Framework and Compliance Requirements for Stability Mechanisms

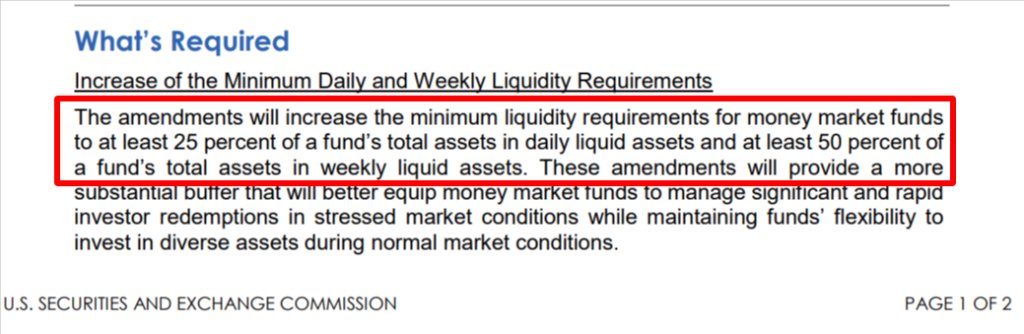

Source from SEC

Man, I still remember the first time my manager handed me a 200-page SEC Rule 2a-7 document and said “figure out how this affects our clients’ money market fund holdings.” That was back in my second year at the bank, and I thought regulations were just boring paperwork. Turns out, these rules are basically the entire backbone keeping money market funds from turning into a Wild West situation.

I spent weeks trying to wrap my head around why we needed so many different regulatory frameworks for what seemed like simple cash management products. But after digging into the 2014 reforms and seeing how they actually work in practice, I get it now.

SEC Rule 2a-7: The Heavy Hitter

The 2014 reforms to Rule 2a-7 completely changed how money market funds operate in the U.S. Before these changes, pretty much all money market funds used a stable $1.00 net asset value. Now we’ve got this whole new world of floating NAV requirements for institutional prime funds.

Here’s what really changed after 2014:

- Floating NAV requirement – Institutional prime and municipal funds must price their shares to four decimal places

- Liquidity fees and gates – Funds can impose fees up to 2% or temporarily halt redemptions if weekly liquid assets fall below 30%

- Enhanced diversification – Stricter limits on exposure to any single issuer

- Stress testing – Monthly assessments of how funds would handle various market scenarios

I’ve had to explain these changes to probably hundreds of clients by now. The floating NAV thing always throws people off because they’re used to that rock-solid $1.00 price.

European MMFR: Different Continent, Different Rules

Working with some international clients taught me that Europe took a completely different approach with their Money Market Fund Regulation that became fully effective in January 2019. The Europeans were way more conservative about the whole thing.

Key Differences Between SEC and European Approaches:

U.S. Approach (Rule 2a-7):

- Allows stable NAV for retail funds

- Liquidity fees and gates as primary tools

- More flexibility in fund structures

- Focus on market-based solutions

European Approach (MMFR):

- Three distinct fund categories with strict requirements

- Public debt CNAV funds (stable NAV) limited to government securities

- Low volatility NAV funds must maintain stable pricing through active management

- Variable NAV funds operate with floating prices

The European rules are honestly more restrictive, but they learned from watching what happened here in 2008. I’ve had clients ask which system is “better,” and there’s no easy answer to that one.

Stress Testing: More Than Just Academic Exercise

I used to think stress testing was just regulatory theater until I saw the actual results from some of the scenarios we run. These tests model everything from interest rate spikes to credit events to massive redemption waves.

Current Stress Testing Requirements:

- Monthly portfolio stress tests examining interest rate and credit spread scenarios

- Redemption stress tests modeling how funds handle large outflows

- Name concentration analysis looking at exposure to individual issuers

- Liquidity stress scenarios testing ability to meet redemption demands

The data from these tests actually drives real business decisions. I’ve seen funds change their entire investment strategy based on stress test results that showed vulnerabilities they didn’t know they had.

Reporting: The Paper Trail That Never Ends

The reporting requirements are honestly overwhelming sometimes. Between Form N-MFP filings, Form N-CR reports, and all the other documentation, fund managers are basically producing a small novel worth of regulatory paperwork every month.

What gets me is how much transparency we have now compared to before 2008. Investors can see exactly what’s in these funds, how liquid the holdings are, and what kind of risks they’re taking on. It’s a massive improvement, even if it creates a ton of work for everyone involved.

Understanding these regulatory frameworks isn’t just about compliance – it’s about recognizing how much the industry learned from past mistakes and how seriously regulators take the stability of these critical funding markets. The rules might be complex, but they’re there for a reason that became crystal clear back in 2008.

Net Asset Value (NAV) Stability and Floating NAV Requirements

Source from SEC

I’ll never forget the first time I had to explain to a client why their “safe” money market fund suddenly had a share price of $1.0023 instead of the usual $1.00. It was about six months into my banking career, and this corporate treasurer was absolutely panicking because their accounting system couldn’t handle fractional pricing. That’s when I really understood why the whole stable versus floating NAV debate isn’t just some technical accounting issue – it literally changes how people use these funds.

Before 2014, pretty much every money market fund in the U.S. used stable NAV pricing. Everyone got comfortable with that nice, predictable $1.00 per share. Then the regulators said “nope, we need more transparency” and everything changed for institutional prime funds.

The Great NAV Structure Divide

After working with dozens of clients through this transition, I’ve seen firsthand how different NAV structures create completely different investor experiences. Let me break down what we’re actually dealing with here:

Stable NAV Funds:

- Eligible fund types: Government funds, retail prime funds, retail municipal funds

- Pricing method: Maintain $1.00 per share using amortized cost accounting

- Investor appeal: Predictable accounting, simplified cash management

- Risk management: Liquidity fees and gates as safety mechanisms

- Technology requirements: Standard transaction processing systems

- Vanguard example: Vanguard Federal Money Market Fund (VMFXX) for government funds and Vanguard Municipal Money Market Fund (VMSXX) for municipal funds

Floating NAV Funds:

- Eligible fund types: Institutional prime funds, institutional municipal funds

- Pricing method: Mark-to-market daily with pricing to four decimal places

- Investor appeal: More transparent risk pricing

- Risk management: Market-based price discovery reduces run risk

- Technology requirements: Real-time valuation and pricing systems

- Note: Vanguard doesn’t currently offer institutional floating NAV funds to retail investors

The weird thing is, both structures are trying to solve the same basic problem – how do you keep money market funds stable without creating moral hazard? They just take totally different approaches to get there.

Mark-to-Market: Reality Check or Unnecessary Volatility?

I spent months helping clients understand what mark-to-market valuation actually means for their day-to-day operations. Basically, instead of using the purchase price of securities (amortized cost), floating NAV funds have to price everything at current market values every single day.

This sounds simple until you realize that money market securities don’t always have active trading markets. I’ve seen our pricing team struggle to find good market data for some commercial paper or certificates of deposit. When you can’t find a real market price, you end up using matrix pricing or dealer quotes, which introduces its own set of complications.

The accuracy question keeps coming up in client meetings. Is a floating NAV actually more “accurate” if it’s based on estimated prices? That’s a philosophical debate I still don’t have a good answer for.

Monitoring NAV Volatility: More Art Than Science

Our risk management team tracks NAV volatility across all the money market funds we recommend to clients. The tools we use include:

- Daily NAV tracking against benchmark rates and peer funds

- Duration risk analysis measuring sensitivity to interest rate changes

- Credit spread monitoring for corporate and bank-issued securities

- Liquidity scoring based on bid-ask spreads and trading volumes

- Stress scenario modeling for various market conditions

What I’ve learned is that even “stable” NAV funds have underlying volatility – you just can’t see it because of the accounting treatment. The floating NAV funds make that volatility visible, which can be jarring for investors who thought they were getting something risk-free.

How Floating NAV Changed Everything

The behavioral changes after the 2014 reforms were honestly more dramatic than anyone expected. I watched our institutional clients completely reorganize their cash management strategies.

Pre-2014 Behavior:

- Clients used prime money market funds like checking accounts

- Large, frequent transactions without price considerations

- Cash management based purely on yield comparisons

- Minimal attention to underlying fund portfolios

Post-2014 Behavior:

- Shift toward government-only funds for operational cash

- More strategic use of prime funds for specific purposes

- Increased focus on liquidity management and timing

- Greater awareness of credit risk in fund holdings

The flow data tells the story – institutional prime fund assets dropped from about $926 billion to around $123 billion after the reforms. That’s not just a regulatory change; that’s a fundamental shift in how people think about cash management.

Technology Infrastructure: The Hidden Complexity

Here’s something most people don’t think about – the technology requirements for floating NAV funds are completely different from stable NAV funds. I worked on a project evaluating different fund platforms for our clients, and the complexity was mind-blowing.

Real-Time NAV Calculation Requirements:

- Integration with multiple pricing vendors for market data

- Automated portfolio valuation systems running throughout the day

- Real-time risk monitoring and compliance checking

- Fractional share accounting and transaction processing

- Detailed audit trails for all pricing decisions

The cost difference is significant too. Some fund companies told us their technology costs increased by 30-40% just to handle floating NAV requirements. That cost ultimately gets passed on to investors through higher expense ratios.

Understanding NAV structures isn’t just about accounting preferences – it’s about recognizing how regulatory changes can completely reshape investor behavior and market dynamics. The floating NAV requirement was supposed to make money market funds safer, but it also made them a lot more complicated to use and manage.

Bottom Line

The money market fund industry has fundamentally transformed since 2008, evolving from a largely unregulated “cash equivalent” investment into a heavily monitored, multi-tiered system with sophisticated risk management tools. While these changes have made the industry more resilient and transparent, they’ve also created a more complex landscape that requires investors to understand the different fund types and their associated risks and benefits.

The shift toward government funds and away from prime funds after the 2014 reforms shows that when given a choice between convenience and perceived safety, institutional investors overwhelmingly choose safety for their cash management needs. This behavioral change, combined with enhanced regulatory oversight and improved stability mechanisms, has reduced systemic risk but also highlighted how regulatory design can have far-reaching unintended consequences on market structure and investor behavior.

Disclaimer: The information provided in this article is for educational purposes only and should not be considered personalized financial advice, as investment decisions should always be based on your individual financial situation and risk tolerance. Past performance and current yields mentioned are not guarantees of future results, and you should consult with a qualified financial advisor before making any investment decisions.