Money Market Fund Tax Traps: What the IRS Won’t Tell You

Are you aware that countless money market fund holders unknowingly trigger tax obligations on investment earnings that could be legally minimized? For the millions of Americans who rely on money market funds as their go-to cash investment, mastering these tax rules can translate into significant savings when April rolls around!

As market uncertainty drives more investors toward stable, accessible investments, choosing from the top money market funds for 2025 while understanding what Wall Street won’t tell you about these investments becomes crucial for tax optimization. From newcomers to experienced investors, this comprehensive guide will reveal the essential tax strategies for money market funds, helping you optimize your returns and minimize what you owe the IRS.

Taxable vs. Tax-Exempt Money Market Funds: Know the Difference

Man, when I first started working at the bank in 2022, I thought all money market funds were basically the same. Boy was I wrong! It wasn’t until I began investing my own money in 2023 that I really understood how much taxes can eat into your returns. Let me tell you, learning this lesson cost me a few hundred bucks that first year.

I remember parking about $15,000 in what I thought was a “safe” money market fund – the Vanguard Federal Money Market Fund (VMFXX). The yield looked great at around 4.2%, but come tax time, I was shocked when I owed Uncle Sam on every penny of interest I earned. That’s when I dove deep into understanding the difference between taxable and tax-exempt money market funds.

How Taxable Money Market Funds Work

Taxable money market funds like VMFXX generate income that’s subject to federal taxes – and usually state taxes too. These funds typically invest in:

- Corporate commercial paper

- U.S. Treasury securities

- Government agency bonds

- Bank certificates of deposit

The interest you earn gets reported on your 1099-DIV, and you’ll pay ordinary income tax rates on it. So if you’re in the 24% federal tax bracket and earned $1,000 in interest, you’re looking at paying $240 in federal taxes alone.

Here’s something that surprised me though – even government money market funds that invest in Treasury securities are only exempt from state taxes in most cases. You still owe federal taxes on the interest.

Municipal Money Market Funds: The Tax-Free Alternative

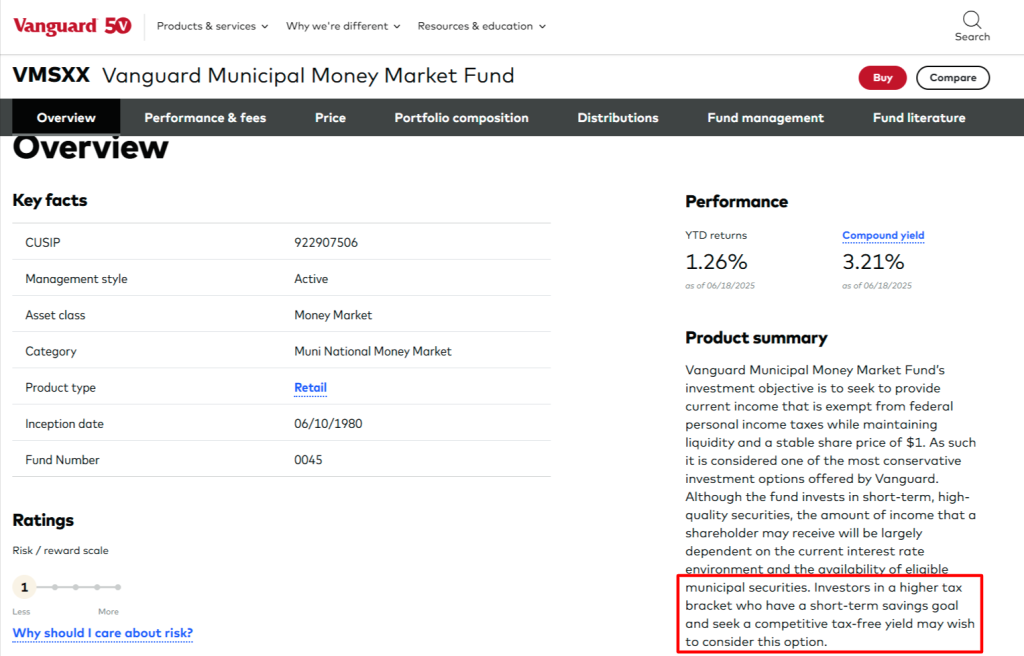

Municipal money market funds are where things get interesting. These funds, like the Vanguard Municipal Money Market Fund (VMSXX) or Fidelity Municipal Money Market Fund (FTEXX), invest in short-term municipal bonds and notes issued by state and local governments.

Key Benefits:

- Interest is exempt from federal income taxes

- May be exempt from state taxes if you live in the issuing state

- Often exempt from Alternative Minimum Tax (AMT)

Typical Yields (as of mid-2025):

- Municipal money market funds: 3.3-3.7%

- Taxable money market funds: 4.2-4.3%

State Tax Implications: Location Matters

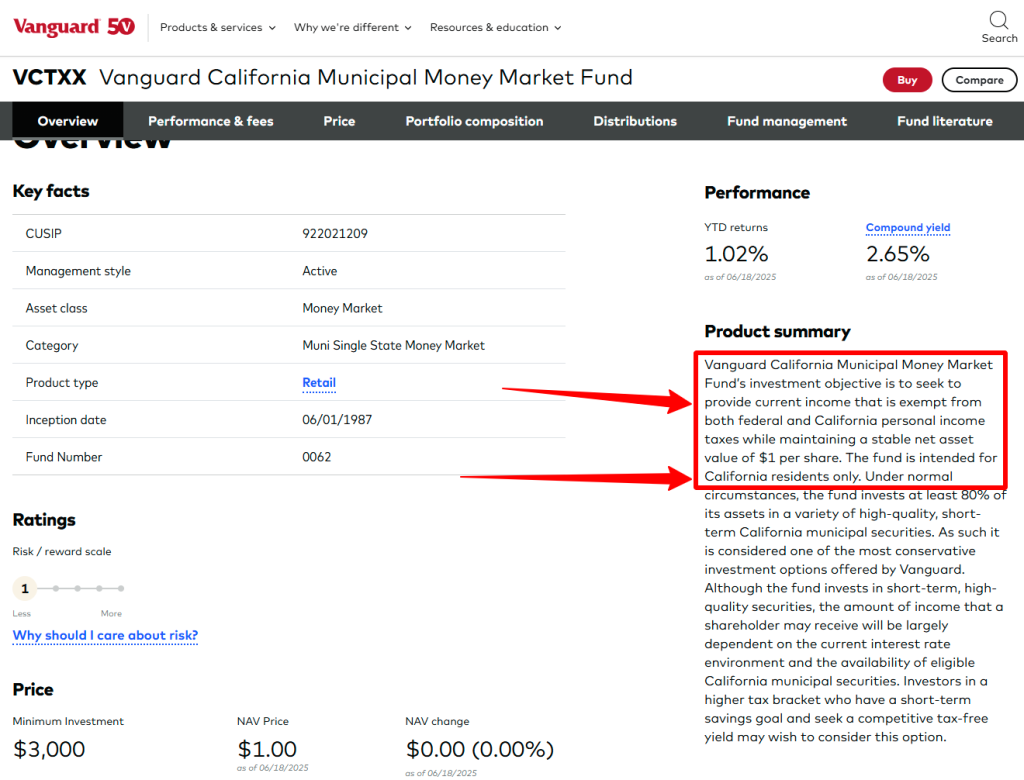

This is where it gets tricky, and honestly, where I made my biggest mistake initially. If you live in a high-tax state like California or New York, state-specific municipal money market funds can be goldmines.

State-Specific Options:

- California residents: Vanguard California Municipal Money Market Fund (VCTXX) – exempt from both federal and California state taxes

- New York residents: Similar funds available for NY municipal securities

- Other states: National municipal funds still provide federal tax exemption

For my California clients, I often run this calculation: if you’re in the 37% federal bracket plus 13.3% California state tax (total 50.3%), a 3.3% tax-free yield is equivalent to about 6.6% in a taxable account. That’s huge!

Alternative Minimum Tax (AMT) Considerations

Here’s something that trips up a lot of people, especially those with higher incomes. Some municipal bonds are subject to AMT, but most money market municipal funds specifically avoid these securities. When researching funds, look for language like “AMT-free” in the fund description.

I learned this the hard way when a client got hit with AMT because they held municipal bonds (not money market funds) that weren’t AMT-free. Always double-check this if you’re subject to AMT.

When Tax-Exempt Might Not Be Your Best Choice

Despite the tax benefits, tax-exempt money market funds aren’t always the winner. Here’s when you might want to stick with taxable options:

- Lower Tax Brackets: If you’re in the 12% federal tax bracket or lower, the after-tax yield on taxable funds often beats tax-exempt funds

- Tax-Advantaged Accounts: In your 401(k), IRA, or Roth IRA, taxes don’t matter, so go for the highest yield

- Short-Term Parking: If you’re only parking cash for a few weeks, the tax difference might be minimal

- State Considerations: If you live in a no-income-tax state like Florida or Texas, national municipal funds lose some appeal

Key Takeaways

After working with hundreds of clients and managing my own investments, here’s my rule of thumb:

For taxable accounts:

- High-tax states (CA, NY, NJ): Consider state-specific municipal money market funds

- Federal tax bracket 22% or higher: Municipal funds usually win

- Lower tax brackets: Run the math, but taxable often comes out ahead

Quick Tax-Equivalent Yield Calculation: Tax-equivalent yield = Municipal yield ÷ (1 – your marginal tax rate)

For example: 3.3% municipal yield ÷ (1 – 0.24) = 4.3% equivalent taxable yield

Don’t just look at the headline yield – always calculate what you actually keep after taxes. That 4.3% taxable yield might look decent, but if you’re only netting 3.3% after taxes, that 3.3% municipal fund suddenly looks pretty attractive.

The key is knowing your tax situation and doing the math. Trust me, your future self will thank you when tax season rolls around!

Strategic Tax Planning for Money Market Fund Holdings

I’ll never forget the call I got from a client in December 2023. She was panicking because her accountant told her she’d owe thousands in taxes on her money market fund interest – money she thought was “safe” from tax complications. That conversation completely changed how I approach money market fund placement with my clients, and honestly, how I manage my own portfolio too.

See, when I started investing in 2023, I made the classic mistake of treating all money market funds the same regardless of what account they lived in. Big mistake! Learning optimal account placement has probably saved me more money than any other strategy I’ve implemented.

Account Placement: The Foundation of Tax Efficiency

Here’s the thing about money market funds – where you hold them matters way more than which specific fund you choose. After working with hundreds of clients and seeing the tax bills, I’ve developed a pretty clear hierarchy.

Tax-Advantaged Accounts (401k, IRA, etc.):

- Prioritize the highest-yielding money market fund

- Tax implications don’t matter since growth is tax-deferred or tax-free

- Perfect spot for taxable money market funds yielding 4.2-4.3%

Taxable Accounts:

- Municipal money market funds for high earners (22%+ tax bracket)

- Treasury money market funds for state tax savings

- Regular money market funds only for lower tax brackets

I learned this lesson personally when I had about $25,000 sitting in the Schwab U.S. Treasury Money Fund (SNSXX) in my taxable account, thinking I was being conservative. Turns out, with my California state taxes, I was leaving money on the table compared to a municipal fund.

Money Market Funds in Retirement Accounts

Using money market funds in your 401k or IRA is actually brilliant for certain situations. Since you’re not paying taxes on the growth anyway, you want maximum yield.

Best Uses for Retirement Account Money Market Funds:

- Emergency cash allocation: Keep 3-6 months expenses in stable value

- Rebalancing buffer: Park proceeds from sales before reallocating

- Dollar-cost averaging: Stage funds for systematic investing

- Pre-retirement transition: Reduce volatility as you approach retirement

I keep about 10% of my 401k in money market funds as a “opportunity fund” – when the market crashes, I’ve got cash ready to deploy. During the March 2024 mini-correction, this strategy paid off big time.

Tax-Loss Harvesting: Money Market Funds Play a Role

Now here’s where it gets interesting. Most people think money market funds can’t lose money, so how do you harvest losses? Well, you can’t directly with the funds themselves, but they play a crucial supporting role in your overall tax-loss harvesting strategy.

How Money Market Funds Support Tax-Loss Harvesting:

Cash Parking for Wash Sale Avoidance:

- Sell losing positions and park proceeds in money market funds

- Wait 31 days to avoid wash sale rules (the wash sale rule prohibits buying the same or substantially identical security within 30 days before or after the sale)

- Redeploy into similar (but not identical) investments

Liquidity for Opportunities:

- Keep harvested losses in money market funds

- Quick access when you spot new tax-loss harvesting opportunities

- No market risk while waiting for the right timing

Important Note: The wash sale rule applies across all your accounts – if you sell a security for a loss in your taxable account and buy the same security in your IRA within 30 days, you’ll lose the ability to claim that tax loss. I’ve seen people try to sell in their taxable account and immediately buy in their IRA thinking they’re clever. Wrong move!

Year-End Tax Planning Strategies

December is always crazy busy at the bank because everyone suddenly cares about taxes. Here’s my year-end money market fund checklist:

November Actions:

- Review taxable account yields vs. tax-equivalent yields

- Calculate potential tax savings from municipal fund switches

- Assess cash needs for tax-loss harvesting in December

December Moves:

- Execute any money market fund swaps (no wash sale issues here)

- Park tax-loss harvesting proceeds in highest-yield money market funds

- Consider Roth conversion opportunities with losses offsetting gains

Real Example from 2024:

- Client had $50,000 in taxable money market fund yielding 4.5%

- Switched to municipal fund yielding 3.4%

- Tax savings: $550 annually (24% federal + 9% state bracket)

Coordination with Fixed-Income Investments

This is where my banking background really helps. Most people think about money market funds in isolation, but they should be part of your broader fixed-income strategy.

Strategic Coordination Approaches:

Bond Ladder Support:

- Use money market funds for the “cash bucket” in bond ladders

- Provides liquidity while waiting for optimal bond purchase timing

- Better than letting cash sit earning nothing

Duration Management:

- Money market funds = zero duration

- Balance against longer-duration bond funds

- Adjust allocation based on interest rate outlook

Credit Quality Diversification:

- Government money market funds = highest credit quality

- Complement with investment-grade corporate bonds

- Municipal money market funds + municipal bond funds for tax efficiency

Account Type Optimization Matrix:

| Account Type | Best Money Market Fund Choice | Why |

| 401k/403b | Highest yielding taxable fund | No tax consequences |

| Traditional IRA | Prime or government funds | Tax-deferred growth |

| Roth IRA | Highest yielding available | Tax-free growth |

| Taxable (High Income) | Municipal funds | Tax exemption benefits |

| Taxable (Lower Income) | Government or prime funds | Higher absolute yields |

My Personal Strategy

Here’s exactly how I structure my money market holdings across accounts:

- 401k: 8% allocation in highest-yield government fund (rebalancing buffer)

- Roth IRA: 5% in prime money market fund (emergency access)

- Taxable: 100% municipal money market fund for cash reserves

- HSA: Small allocation in Treasury fund (triple tax advantage)

The key is thinking holistically about your entire portfolio, not just individual accounts. Every dollar should be working as hard as possible within its tax environment.

Remember, optimal money market fund placement isn’t sexy, but it’s the foundation of tax-efficient investing. Get this right, and everything else becomes easier.

Bottom Line

After diving deep into the world of money market fund taxation, one thing becomes crystal clear: the devil is truly in the details. What seems like a simple cash parking decision can easily cost you hundreds or thousands of dollars in unnecessary taxes if you’re not paying attention to account placement and fund selection.

The biggest mistake I see investors make is treating all money market funds the same, regardless of their tax situation or the account type they’re using. Don’t be that person who discovers in April that they’ve been paying Uncle Sam far more than necessary all year long.

Here’s the bottom line: know your tax bracket, understand where your money is parked, and do the math before you invest. Whether you’re earning 4.2% in a taxable fund or 3.3% in a municipal fund, what matters most is what you get to keep after taxes. Smart money market fund selection isn’t just about yield – it’s about building a tax-efficient foundation that lets your entire investment strategy work harder for you.

Disclaimer: The information provided in this article is for educational purposes only and should not be considered personalized financial advice, as investment decisions should always be based on your individual financial situation and risk tolerance. Past performance and current yields mentioned are not guarantees of future results, and you should consult with a qualified financial advisor before making any investment decisions.