Money Market Funds in 401k: Safe or Sorry Investment?

Can you believe that while target-date funds dominate 401k allocations (with nearly 95% of participants using them), many people still keep portions of their retirement savings in conservative options like money market funds? When choosing between the best money market funds for 2025, it’s essential to understand what Wall Street won’t tell you about how these investments actually work within your 401k plan.

If you’ve ever stared at your 401k investment menu feeling overwhelmed by choices, you’re not alone. This comprehensive guide will break down everything you need to know about money market funds in your 401k plan, helping you decide if they deserve a spot in your retirement portfolio.

The Major Advantages of Money Market Funds in Your 401k

Man, I wish someone had explained money market funds to me when I first started investing back in 2023. I was one of those people who thought you just threw everything into aggressive growth stocks and called it a day – until I started learning about market history and realized how brutal crashes like 2008 and 2022 were for people close to retirement.

That’s when my financial advisor friend (bless her heart) sat me down and explained money market funds. Honestly, I thought they sounded boring as heck at first. But after researching what happened to people who lost 20-40% of their portfolio value right before retirement, boring started looking pretty darn attractive.

Capital preservation and principal protection benefits

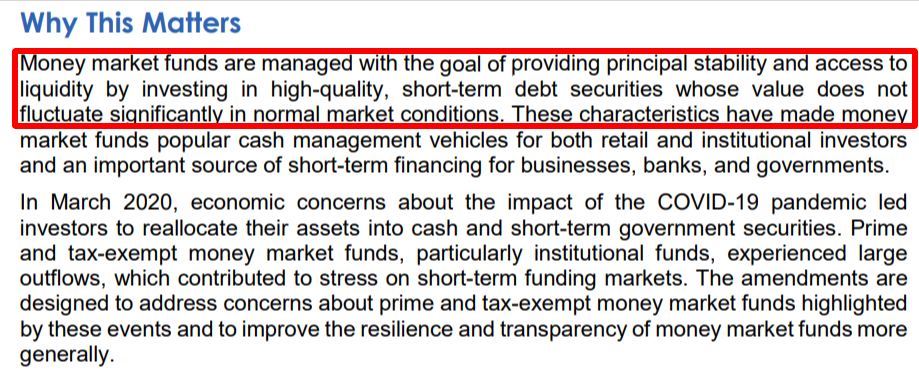

From SEC website

The biggest game-changer for me was understanding the capital preservation aspect. Unlike growth stocks that can bounce around like a pinball machine, money market funds keep your principal safe. Yeah, the returns aren’t gonna make you rich overnight, but you’re not losing sleep either. Most money market funds aim to maintain a stable $1.00 net asset value per share, which means your initial investment stays put (not guaranteed but less likely to break).

The liquidity thing is huge too, and I learned this through research rather than painful experience. When you want to rebalance your portfolio during market volatility, you can get stuck waiting for settlement periods on some investments. But with money market funds? You can move that money around same-day. No redemption fees, no waiting periods – just clean, simple transfers.

Professional money management and diversification

Here’s what really impressed me though – the professional management part. I used to think I was smart enough to pick my own investments (jury’s still out on that one). Money market funds have actual professionals managing a diversified portfolio of short-term securities like treasury bills, commercial paper, and certificates of deposit. These aren’t some random people picking stocks; they’re specialists who understand credit risk and interest rate movements way better than I ever will.

The volatility difference is night and day. While stock funds can swing 20-30% in either direction, money market allocations barely budge. During 2023 and early 2024, when markets were choppy due to interest rate concerns, money market funds actually earned decent returns thanks to higher rates, with many offering yields above 4%. For example, VMFXX (Vanguard Federal Money Market Fund) has been offering competitive yields while maintaining its focus on government securities and high-quality short-term investments.

Now, about insurance protection – this is where it gets a little tricky. Money market funds themselves are not FDIC insured, but they may be eligible for SIPC coverage (up to $500,000) when held in a brokerage account. Some 401k providers offer FDIC-insured deposit sweep programs that can provide additional protection, but you gotta read the fine print on this one. I made sure to dig through my plan documents to understand exactly what protection I had.

Predictable returns and income generation

The predictable income aspect is really appealing as I think about long-term retirement planning. Instead of wondering if dividends will get cut or bond funds will tank, you know roughly what you’re getting each month. It’s not exciting, but it’s reliable – kinda like that old Honda that just keeps running.

During market uncertainty, money market funds can serve as your “parking spot.” When everything feels crazy and you don’t know what to buy, you can temporarily move funds there while you figure things out. No pressure, no timing the market – just a safe place to sit tight.

The diversification aspect really makes sense when you think about banking risks. While people worry about individual bank failures, money market funds are spread across dozens of different institutions and securities. When regional banks had troubles in early 2023, well-managed money market funds barely felt a blip because fund managers limit exposure to any single institution.

What really opened my eyes was learning about the different types of securities these funds hold. We’re talking treasury bills with maturities under a year, high-grade commercial paper from solid companies like Microsoft and Johnson & Johnson, and repurchase agreements backed by government securities. This stuff is way more sophisticated than it initially sounds.

The Significant Drawbacks You Need to Consider

Okay, real talk time. After learning about the benefits of money market funds, I gotta be honest about where they absolutely fall short – and these are lessons I’ve learned through research and talking to people who’ve been through multiple market cycles.

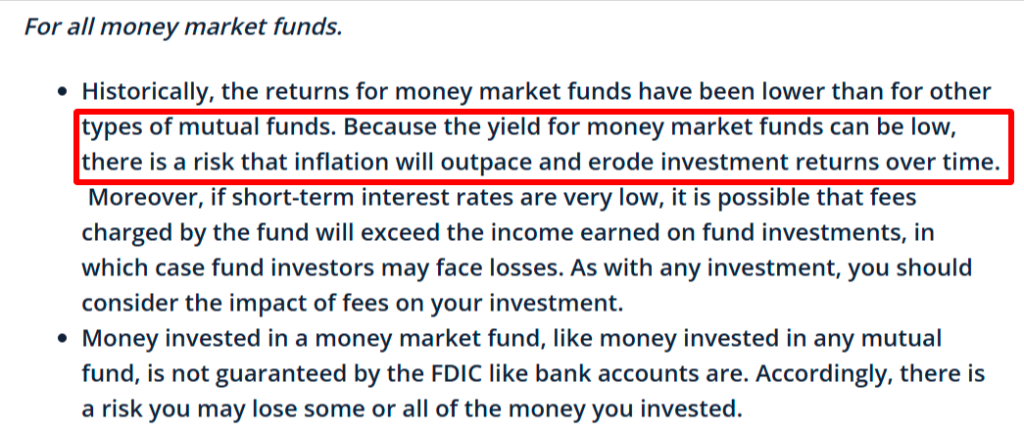

Low returns that may not keep pace with inflation

From investor.gov

The biggest concern is watching inflation eat your returns. When I look at recent history, like 2019 when money market funds were earning around 2.2% annually while inflation was running about 1.8%, you’re barely staying ahead of the inflation curve. During high inflation periods like 2021-2022, when inflation hit over 8%, money market returns got crushed in real terms.

Here’s where it gets really painful: opportunity cost. People who played it “safe” with big chunks in money market funds from 2010 to 2020 missed out on the S&P 500’s compound annual returns that often exceeded 10%. I know folks who could have retired years earlier if they’d been more aggressive during their prime earning years.

Limited growth potential for long-term retirement goals

The long-term growth limitation is brutal for retirement planning. I ran some numbers that made me sick to my stomach. If someone kept 40% of their 401k in money market funds over a 30-year career, they’d have hundreds of thousands less at retirement compared to a more aggressive allocation. That’s potentially years of extra work needed.

Interest rate risk is tricky to understand. When rates fall, money market yields drop quickly. When rates were near zero in 2020-2021, these funds earned practically nothing while bond prices actually went up. You can get stuck earning minimal returns while other “safe” investments gain value.

Those management fees are sneaky wealth killers. Most money market funds charge between 0.15% and 0.75% annually in expense ratios. On a $100,000 balance earning 4%, that fee takes away 15-20% of your total returns. Over decades, that’s serious money lost to compound growth.

No tax advantages beyond standard 401k benefits except for Muni-bond funds

The tax situation depends on the type of money market fund. Most regular money market funds get the same tax deferral as any other 401k investment, but municipal money market funds can offer additional benefits. Municipal money market funds invest in tax-free municipal bonds, which means the interest income is typically exempt from federal taxes (and sometimes state taxes too). In a Roth 401k, this creates a “double tax advantage” – tax-free municipal interest plus tax-free withdrawals in retirement. However, in a traditional 401k, the municipal tax advantage is somewhat diminished since you’ll pay ordinary income tax on withdrawals anyway. Still, municipal money market funds can be more tax-efficient than regular money market funds, especially if your plan offers them.

But here’s the real kicker: purchasing power erosion over decades. Historical data shows that if inflation averages 3% annually and your money market fund earns 4%, you’re only gaining 1% in real purchasing power. That’s not enough for building serious wealth.

The comfort trap is real too. It’s easy to get too comfortable with money market funds after learning about market crashes, but staying too conservative for too long can cost you dearly in missed gains during bull markets.

When Money Market Funds Make Sense in Your 401k Strategy

Look, after diving deep into investment research and talking to financial advisors, I’ve figured out when money market funds actually make sense. Like most things in life, it’s not all-or-nothing.

Pre-retirement phase (ages 55-65) asset allocation considerations

The pre-retirement phase is where money market funds really shine. Financial advisors consistently say that when you’re within 5-10 years of retirement, you can’t afford to risk a major market crash wiping out 30% of your nest egg. That’s when gradually shifting 20-25% of your portfolio into money market funds and stable value options makes sense.

Here’s the thing about being close to retirement – you don’t have time to recover from major market crashes. People who lost significant money in 2008 at age 62 had to delay retirement by years just to get back to even. Research shows that older workers increased their expected retirement age by about 2.5 months on average due to wealth losses from the 2008 crisis. A more conservative allocation might only drop 8-10% during market crashes instead of 30-40%.

Money market funds work great as an emergency fund alternative when you’re over 59½. Before that age, you’ll get hit with penalties for early withdrawals, but once you clear that hurdle, having 6-12 months of expenses in your 401k money market fund beats keeping it in a regular savings account earning minimal interest.

Risk tolerance assessment and conservative investor profiles

Risk tolerance changes as you get older and your time horizon shortens. If large portfolio swings make you anxious and lead to bad decisions, having 15-20% in money market funds can give you the peace of mind to keep the rest invested aggressively.

Short-term goals within your 401k are perfect for money market allocation. If you’re planning major expenses in retirement that you’ll fund from your 401k, moving that money into stable investments 12-18 months beforehand protects it from market corrections.

The rebalancing strategy makes a lot of sense. Instead of selling winners to buy losers (which feels awful), you can use money market funds as a staging area. When your stock allocation gets too high, take profits into the money market fund. Then when stocks drop, you’ve got cash ready to deploy.

Having some allocation in money market funds can help you sleep at night during bear markets. Sometimes boring is exactly what you need to stay disciplined with your overall investment strategy.

Bottom Line

After digging through all this research, here’s my honest take: money market funds aren’t the star player in your 401k, but they definitely have a role on the bench. They’re like that reliable friend who’s not the most exciting person at the party, but you know you can count on them when things get crazy.

The key is understanding when to use them and when to avoid them like yesterday’s leftovers. If you’re young and have decades until retirement, keeping more than 5-10% in money market funds is probably costing you serious money in the long run, but as you get closer to retirement, they can provide the peace of mind that actually helps you stay more aggressive with the rest of your portfolio.

Disclaimer: The information provided in this article is for educational purposes only and should not be considered personalized financial advice, as investment decisions should always be based on your individual financial situation and risk tolerance. Past performance and current yields mentioned are not guarantees of future results, and you should consult with a qualified financial advisor before making any investment decisions.