Money Market Funds Recession Test: Do They Really Work?

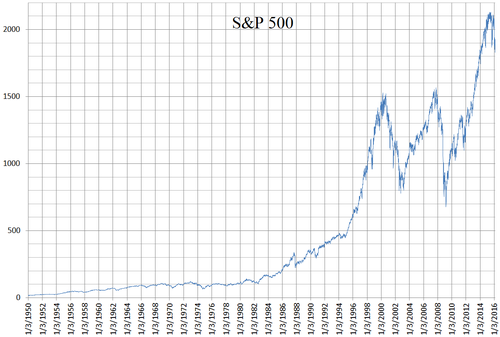

When the 2008 financial crisis sent the S&P 500 crashing 57%, money market funds remarkably maintained their value throughout the turmoil. This performance track record explains why understanding the top money market funds for 2025 has become crucial for investors seeking stability in today’s volatile market environment.

As we navigate 2025’s uncertain economic landscape, you’re probably wondering: are money market funds truly recession-proof? While what Wall Street won’t tell you about money market funds reveals some surprising limitations, these conservative investments have historically served as a financial lighthouse during economic turbulence, offering stability when markets get choppy and providing liquidity when other investments freeze up.

Historical Performance of Money Market Funds During Past Recessions

You know, when I first started digging into money market fund research at the bank in 2022, I honestly thought these things were bulletproof. Like, completely recession-proof investments that just chugged along no matter what the economy threw at them. Boy, was I in for some eye-opening discoveries when I started pulling historical data for client presentations.

My manager actually assigned me to research this exact topic when we had a bunch of nervous clients asking about “safe” investments during all the 2022 market volatility. I spent weeks going through performance data, and what I found completely changed how I think about money market funds during economic downturns.

The 2008 Great Recession: A Wake-Up Call

Lehman Brothers

The 2008 crisis was probably the most dramatic test for money market funds in recent history. Before this, most people (including seasoned bankers at my firm) thought these funds were essentially risk-free. The Reserve Primary Fund breaking the buck in September 2008 shattered that illusion pretty quickly.

Here’s what actually happened during that period:

Traditional Money Market Fund Performance (2008-2009):

- Average 7-day yield dropped from around 5.0% in early 2008 to near 0.1% by late 2009

- Most government funds maintained $1.00 NAV but yields plummeted

- Prime funds faced significant redemption pressure and credit concerns

- Institutional funds saw massive outflows as companies pulled cash

I remember looking at Vanguard’s Prime Money Market Fund (VMMXX) data from that period and being shocked. Even though it maintained its $1 NAV, the yield went from over 4% to basically zero within months. Meanwhile, government-focused funds like Fidelity’s Government Money Market Fund (SPAXX) actually saw inflows as investors fled to safety.

The real lesson? Money market funds don’t lose principal (usually), but their yields can crater during recessions when the Fed cuts rates aggressively.

Dot-Com Bubble and Early 2000s Recession

This period was fascinating to research because it showed a completely different pattern. The 2001-2002 recession was more of a slow burn compared to 2008’s sudden shock.

Performance Comparison: Dot-Com Era vs. 2008

| Metric | 2001-2002 Recession | 2008-2009 Crisis |

| Fed Funds Rate Drop | 6.5% to 1.75% (then 1% by 2003) | 5.25% to 0-0.25% |

| Avg. MMF Yield Decline | ~5.5 percentage points | ~4.8 percentage points |

| Time to Bottom | 24 months | 12 months |

| Principal Losses | Virtually none | Reserve Primary Fund |

What struck me most was how money market funds actually provided decent returns early in the dot-com recession. Schwab’s Value Advantage Money Fund (SWVXX) was yielding over 6% in early 2001 – not bad when tech stocks were getting hammered.

The gradual rate-cutting cycle meant investors could actually capture some yield for longer compared to 2008’s rapid descent to zero.

The Forgotten 1990-1991 Recession

Here’s where my research got really interesting. This recession barely registers on most people’s radar, but it was actually a great case study for money market performance in a “normal” downturn.

Back then, money market funds were still relatively new products, but the ones that existed performed exactly as advertised. The Fed had raised rates to 9.75% by May 1989 to combat inflation, then cut them as the recession hit, reaching 3% by September 1992. There wasn’t the panic or structural issues we saw later.

I found data showing that funds maintained steady asset levels throughout this period. No breaking the buck, no massive redemptions – just gradually declining yields as rates fell.

Stock Market Comparison: The Real Eye-Opener

This comparison really drives home why clients were asking about money markets in the first place:

Total Returns During Major Recessions:

- 2008-2009: S&P 500 down 57% peak-to-trough, money markets maintained capital

- 2001-2002: S&P 500 down 49% over three years, money markets positive (declining yields but no losses)

- 1990-1991: S&P 500 down 20%, money markets stable throughout

But here’s the thing my clients often miss – during recovery periods, they completely missed out on gains. While the S&P bounced back 26% in 2009, money market investors were stuck earning basically nothing.

The COVID-19 Disruption: A Modern Test Case

Since I was actually working during this period, I got to see the 2020 response in real-time. It was wild – the Fed cut rates to zero faster than ever before, and money market yields followed immediately.

What was different this time was the scale of government intervention. Funds like iShares Core High Dividend ETF weren’t even on clients’ radars – they wanted pure safety.

The big government funds actually benefited from flight-to-quality flows, while prime funds again faced pressure from credit concerns.

Risks and Limitations of Money Market Funds During Recessions

When I first started explaining money market funds to clients back in 2022, I used to call them “the boring safe option.” Man, was I oversimplifying things. It wasn’t until I had to deal with a really upset client during one of our quarterly reviews that I realized how many hidden risks these “safe” investments actually carry during economic downturns.

This client had parked about $500,000 in money market funds thinking they were getting a recession-proof investment. Six months later, they were furious about their returns and feeling like they’d been misled. That conversation taught me I needed to dig way deeper into the actual limitations of these funds.

Interest Rate Risk: The Silent Killer

Here’s something that shocked me when I first researched it – money market funds face massive interest rate risk, just in the opposite direction from bonds. When rates fall during recessions (which they almost always do), your income gets absolutely crushed.

Let me break down what I’ve seen happen:

Interest Rate Impact on Money Market Yields:

- 2008-2009: Average yields dropped from 5.2% to 0.1% (98% decline)

- 2020 COVID response: Yields fell from 1.6% to 0.01% in just 8 weeks

- 2001-2002: Gradual decline from 6.1% to 0.8% over 18 months

I remember pulling up Fidelity’s Government Money Market Fund (SPAXX) historical data and showing clients how their $100,000 went from earning $5,200 annually to basically $100. It’s technically not a “loss,” but tell that to someone counting on that income for expenses.

The Fed’s recession playbook is pretty predictable – cut rates aggressively to stimulate the economy. Your money market fund income becomes collateral damage.

Credit Risk: The Hidden Landmine

This one really opened my eyes after studying the 2008 crisis. Most people think money market funds only buy super-safe stuff, but prime funds can hold commercial paper, bank CDs, and corporate debt. During recessions, this credit exposure can bite you hard.

Credit Risk Breakdown by Fund Type:

| Fund Type | Primary Holdings | Credit Risk Level | 2008 Experience |

| Government | Treasury bills, agency debt | Minimal | Stable throughout |

| Prime | Corporate paper, bank CDs | Moderate to High | Reserve Primary broke buck |

| Municipal | Short-term muni bonds | Variable by issuer | Some stress but stable |

The Reserve Primary Fund disaster happened because they held Lehman Brothers commercial paper. When Lehman collapsed, the fund couldn’t maintain its $1.00 share price. I always tell clients now – if you’re worried about recession, stick with government funds like Vanguard Federal Money Market Fund (VMFXX).

Prime funds might offer slightly higher yields during good times, but that extra 0.2% isn’t worth the sleepless nights when credit markets freeze up.

Inflation Risk: The Slow Burn

This risk doesn’t get enough attention, and it’s been brutal for money market investors lately. During recessions, central banks often keep rates artificially low for years afterward. Your money stays “safe” but loses purchasing power steadily.

I calculated this for a client who kept $200,000 in money markets from 2010-2015:

- Annual inflation averaged 2.1%

- Money market yield averaged 0.05%

- Real purchasing power lost: approximately $20,000 over five years

It’s death by a thousand cuts. You’re not losing money on paper, but you’re definitely getting poorer in real terms.

Opportunity Cost: The Biggest Risk Nobody Talks About

Here’s where I really learned my lesson about positioning these funds correctly. During the 2020 recovery, while my clients’ money market funds were earning practically nothing, the stock market went on an absolute tear.

Recovery Performance Comparison (2020-2022):

- S&P 500 total return: +61.8%

- Schwab Value Advantage Money Fund (SWVXX): +0.2%

- Opportunity cost for $100,000: Over $60,000 in missed gains

I had clients who stayed in money markets way too long because they were scared of another crash. Their “safe” choice ended up being incredibly expensive.

Fee Erosion in Low-Rate Environments

This one caught me completely off guard during my first year. When yields drop below expense ratios, funds either waive fees or investors actually lose money. It’s nuts.

Most money market funds have expense ratios between 0.15% and 0.50%. When yields fell to near zero in 2020, some funds were literally paying investors to keep their money just to avoid negative returns. Fund companies ate millions in fee waivers.

Fee Impact Examples:

- Fund with 0.25% expense ratio earning 0.10% = -0.15% real return

- $50,000 investment losing $75 annually after fees

- Many funds waived fees completely rather than show negative returns

Liquidity Restrictions: When “Liquid” Isn’t

The 2008 crisis taught everyone that money market funds can impose restrictions during stress. Some funds limited redemptions or imposed redemption fees when everyone wanted out at once.

I always warn clients that while money market funds are generally liquid, during extreme market stress, that liquidity might not be there when you need it most. It’s rare, but it can happen.

Bottom Line

After digging deep into decades of money market fund performance during recessions, I’ve learned that these “safe” investments are far more complex than most people realize. They absolutely serve a crucial role during economic turbulence – maintaining principal and providing liquidity when everything else is falling apart – but they’re not the recession-proof fortress many investors imagine them to be.

The bottom line? Money market funds are excellent for preserving capital during the chaos of a recession, but they come with their own set of trade-offs that can be surprisingly painful. Your money stays safe, but your income disappears, inflation eats away at your purchasing power, and you miss out on recovery gains that could set you up for years to come.

Disclaimer: The information provided in this article is for educational purposes only and should not be considered personalized financial advice, as investment decisions should always be based on your individual financial situation and risk tolerance. Past performance and current yields mentioned are not guarantees of future results, and you should consult with a qualified financial advisor before making any investment decisions.