Money Market Funds: What Wall Street Won’t Tell You

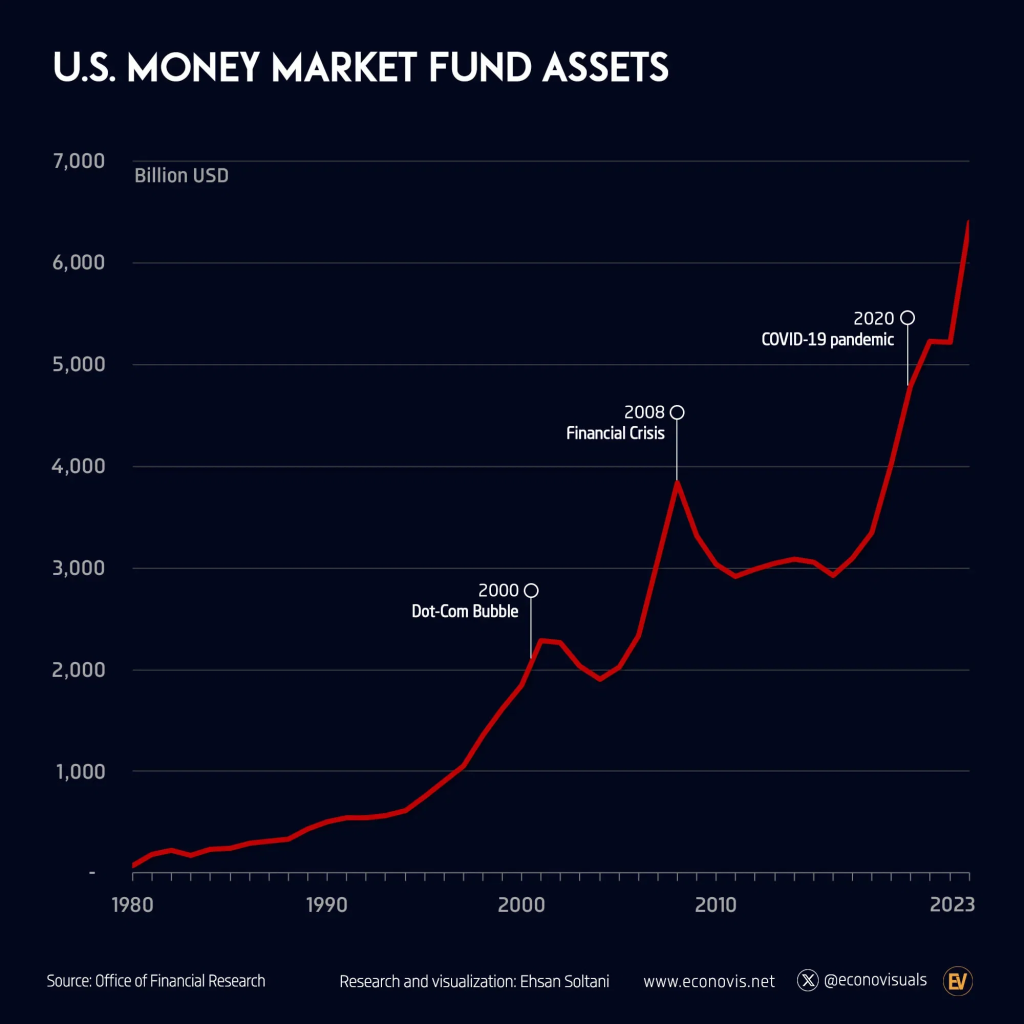

Here’s a shocking truth: 73% of investors have never heard of money market funds, yet these instruments manage over $6 trillion in assets! Wall Street loves keeping these funds under the radar because informed investors are less likely to pay for expensive financial advice and high-fee products. Whether you’re exploring the best money market funds at Charles Schwab, top-performing Fidelity options, or Vanguard’s excellent lineup, understanding these powerful tools can transform your cash management strategy.

What if I told you that money market funds could be your secret weapon for building wealth? These aren’t just boring cash equivalents – they’re sophisticated investment vehicles that can help you beat inflation while keeping your money safe and accessible.

The Money Market Fund Basics Wall Street Doesn’t Want You to Know

What Money Market Funds Really Are

I wish someone had properly explained money market funds when I started at the bank in 2022. I spent months thinking they were just fancy savings accounts with better rates.

Here’s what blew my mind: money market funds aren’t bank accounts at all. They’re mutual funds that invest in super short-term debt securities. When you invest, you’re buying fund shares, not making a deposit. The fund pools everyone’s money to buy Treasury bills, commercial paper, and CDs maturing under 397 days.

This difference is huge. Bank accounts have FDIC insurance up to $250,000. Money market funds don’t—they’re SEC-regulated and while incredibly safe, there’s no government guarantee. They may get $500,000 SIPC coverage in brokerage accounts, but that protects against broker failure, not investment losses. I panicked when I first learned this, but after researching hundreds of these funds for clients, the risk is minimal for quality funds.

Why Financial Advisors Rarely Recommend Them

This is where things get a bit frustrating, and I’m gonna be honest with you. Most financial advisors don’t push money market funds because… well, there’s not much money in it for them. The expense ratios are tiny – we’re talking 0.10% to 0.50% annually – which means lower commissions and fees.

I’ve sat in meetings where advisors steered clients toward more complex products that paid better commissions instead of suggesting the simple money market fund that would’ve been perfect. It’s not necessarily malicious, but advisors have bills to pay too.

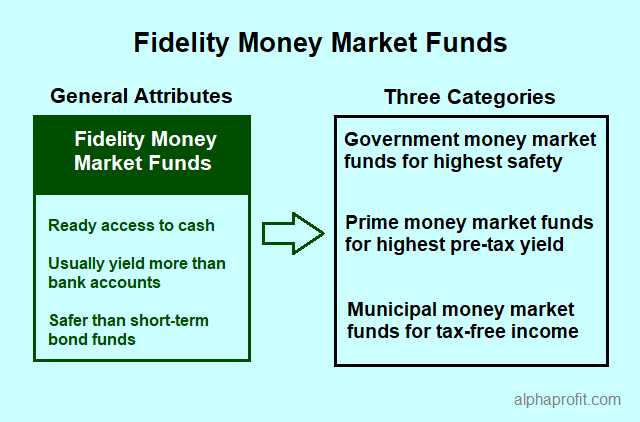

The Three Types of Money Market Funds

Through my work analyzing these products, I’ve learned there are three main flavors, and picking the wrong one can cost you:

Government Money Market Funds

- Invest only in U.S. Treasury securities and government agency debt

- Lowest yields but highest safety

- Best for: Ultra-conservative investors or those needing maximum security

Prime Money Market Funds

- Can invest in corporate debt, bank CDs, and commercial paper

- Higher yields but slightly more risk

- Best for: Most individual investors seeking better returns with acceptable risk

Municipal Money Market Funds

- Focus on short-term municipal securities

- Tax advantages for certain income brackets

- Best for: High earners in states with income tax

When I first started investing in 2023, I made the rookie mistake of chasing the highest yield without considering the fund type. I threw money into a prime fund during a period of banking stress and watched my returns fluctuate more than I expected. Not a disaster, but definitely a learning experience.

For most people, prime funds from established companies like Vanguard’s VMFXX or Fidelity’s SPAXX offer the sweet spot of decent yields with reasonable stability.

How Money Market Funds Generate Returns

The Short-Term Securities That Power These Funds

Okay, this is where it gets interesting. When I first started digging into what money market funds actually buy, I was surprised by the variety. These aren’t just parking money in a bank account – fund managers are actively shopping for the best short-term deals in the market.

Here’s what’s typically in the portfolio:

- Treasury Bills: Government IOUs that mature in 4 weeks to 1 year

- Commercial Paper: Short-term corporate debt (usually 30-270 days)

- Certificates of Deposit: Bank CDs with maturities under 397 days

- Repurchase Agreements: Overnight loans backed by government securities

- Banker’s Acceptances: Trade financing instruments (less common now)

The fund managers are constantly buying and selling these securities as they mature. When a 30-day Treasury bill comes due, they reinvest that money into whatever’s offering the best rate at that moment. It’s like having a professional bargain hunter managing your cash.

Why Your Returns Fluctuate (And Why That’s Actually Good)

This used to confuse the hell out of me. Why does my money market fund yield change every month when my savings account stays the same?

The answer clicked when I realized that fluctuation is actually a feature, not a bug. Your savings account rate is set by the bank and changes only when they feel like it (usually long after market rates move). Money market funds, on the other hand, reflect what’s actually happening in the short-term lending markets right now.

I tracked this during 2023 when the Fed was raising rates aggressively:

- My bank savings account: Went from 0.05% to 0.50% over 12 months (took forever to adjust)

- Vanguard VMFXX: Went from 0.25% to 5.2% in the same period (adjusted monthly)

- The difference: I earned an extra $470 on a $10,000 balance by using the money market fund

The fluctuation means you’re getting paid current market rates, not whatever your bank decides to offer. When rates go up, you benefit quickly. When they go down… well, at least you got the higher rates while they lasted.

The Role of Interest Rates in Your Potential Profits

Here’s something I learned the hard way: money market funds are incredibly sensitive to interest rate changes, but in a good way if you understand the timing.

When the Federal Reserve raises rates, money market funds are usually among the first to reflect those changes. The short maturation periods mean fund managers are constantly reinvesting at new, higher rates. But here’s the kicker – it’s not immediate.

How the timeline typically works:

- Week 1-2: Fed announces rate hike

- Week 3-4: Treasury bill rates adjust

- Month 2: Money market fund yields start climbing

- Month 3: Full impact shows up in your returns

I remember getting frustrated in early 2023 when the Fed raised rates but my Schwab SNSXX fund didn’t budge immediately. Patience paid off though – within 6 weeks, the yield had jumped from 3.1% to 4.2%.

The opposite happens when rates fall. During rate cuts, money market funds will see declining yields as their holdings mature and get reinvested at lower rates. This is actually when you might want to consider locking in longer-term rates with CDs or Treasury bills if you think rates have peaked.

Pro tip from my experience: Don’t try to time the market perfectly with money market funds. The yields adjust relatively quickly, and you’ll drive yourself crazy trying to predict Fed moves. I use them as a parking spot for cash I need within the next 12 months, regardless of where I think rates are heading.

The beauty of money market funds is their simplicity once you understand the basics. They’re not trying to beat the stock market – they’re trying to give you the best possible return on cash while keeping it accessible. And unlike what some advisors might tell you, that’s exactly what many of us need for a portion of our money.

Smart Strategies for Choosing the Right Money Market Fund

Risk Assessment Beyond the Marketing Brochure

I learned this lesson the hard way in March 2023. I was chasing yields like a rookie and threw $8,000 into what I thought was a “safe” money market fund because the marketing materials kept using words like “stable” and “conservative.” Then Silicon Valley Bank collapsed, and my fund’s value dropped 2% in two days because it held a bunch of bank commercial paper.

That wake-up call taught me to look beyond the glossy brochures and actually understand what I was buying. The marketing departments make everything sound bulletproof, but the reality is more nuanced.

Government vs. Prime vs. Municipal Funds: Real Risk Differences

When I first started analyzing these funds for clients, I thought the risk differences were minimal. Wrong. Here’s what I’ve learned from reviewing hundreds of fund portfolios:

Government Money Market Funds

- Risk Level: Practically zero (as close as you can get)

- What They Hold:

- U.S. Treasury bills and notes

- Government agency securities (Fannie Mae, Freddie Mac)

- Repurchase agreements backed by government securities

- Pros:

- Essentially backed by the full faith and credit of the U.S. government

- No credit risk from corporate defaults

- Most stable during market stress

- Cons:

- Lowest yields (typically 0.10-0.30% below prime funds)

- Less flexibility for fund managers to seek higher returns

Prime Money Market Funds

- Risk Level: Low to moderate (depending on holdings)

- What They Hold:

- Corporate commercial paper

- Bank certificates of deposit

- Asset-backed commercial paper

- Some government securities

- Pros:

- Higher yields than government funds

- Professional management seeking best short-term rates

- Diversified across multiple sectors

- Cons:

- Exposed to corporate credit risk

- Can lose value during banking stress or credit crunches

- More volatile during economic uncertainty

Municipal Money Market Funds

- Risk Level: Low to moderate (varies by state/issuer)

- What They Hold:

- Short-term municipal bonds

- Variable rate demand notes

- Tax anticipation notes from cities and states

- Pros:

- Tax-free income (federal, sometimes state)

- Good for high-income investors

- Support local government projects

- Cons:

- Lower pre-tax yields

- Concentrated geographic risk

- Less liquidity than other types

My personal experience? I keep my emergency fund in Vanguard’s government fund VMFXX and use prime funds like Fidelity’s SPAXX for money I’m parking temporarily.

How to Evaluate Credit Quality Without a Finance Degree

This was intimidating at first, but I’ve found some simple ways to assess fund quality without getting a CFA:

Look at the Fund’s WAM (Weighted Average Maturity)

- Under 60 days = Very conservative

- 60-90 days = Moderate

- Over 90 days = More aggressive (higher risk/reward)

Check the Top Holdings Most funds list their top 10-20 holdings. Look for:

- What percentage is in government securities vs. corporate paper

- Are there any names you don’t recognize?

- How concentrated are the holdings? (diversification is good)

Read the Annual Report Summary I know it sounds boring, but spend 10 minutes scanning the manager’s letter. They’ll usually mention any credit issues or portfolio changes.

Red Flags That Signal a Fund Might Be Too Risky

Through my work, I’ve identified several warning signs that scream “stay away”:

Red Flag #1: Yields Significantly Above Peers If a fund is yielding 1%+ more than similar funds, there’s usually a reason. Higher risk, longer maturities, or lower credit quality.

Red Flag #2: High Concentration in One Sector I saw a fund in 2023 that had 40% of its assets in commercial paper from regional banks. When banking stress hit, guess what happened?

Red Flag #3: Frequent Management Changes If the portfolio manager has been there less than two years or there’s been multiple changes recently, that’s concerning.

Red Flag #4: Unusual Holdings for the Fund Type Government funds should hold government securities. If you see corporate paper in there, something’s wrong.

Red Flag #5: Poor Liquidity Terms Some funds have restrictions on withdrawals or minimum holding periods. Money market funds should be liquid.

Yield Comparison Tactic

Why the Highest Yield Isn’t Always the Best Choice

This mistake cost me about $200 in 2023, and I see clients make it all the time. I was comparing three funds and automatically picked the one with the highest 7-day yield. Seemed logical, right?

Wrong. Here’s what I missed:

- Fund A: 5.2% yield, 0.08% expense ratio, government securities

- Fund B: 5.4% yield, 0.45% expense ratio, mixed corporate paper

- Fund C: 5.6% yield, 0.52% expense ratio, heavy bank exposure

I chose Fund C because of that 5.6% yield. Then bank stress hit the market, and Fund C’s yield dropped to 4.8% while Fund A stayed steady at 5.1%. Over six months, Fund A actually outperformed despite the lower starting yield.

What to Look at Instead of Just Yield:

- Consistency: How stable has the yield been over 12 months?

- Quality: What’s the average credit rating of holdings?

- Fees: What’s the net yield after expenses?

- Volatility: How much does the share price fluctuate?

How to Calculate Your After-Tax Returns Effectively

This is where things get interesting, especially if you’re in a higher tax bracket. I learned this when helping a client who was in the 32% federal tax bracket compare options.

The Basic Formula: After-tax yield = Yield × (1 – Your tax rate)

Real Example from My Client:

- Taxable Prime Fund: 5.2% yield

- Municipal Fund: 3.8% yield

- Client’s tax rate: 32% federal + 5% state = 37%

After-tax comparison:

- Prime fund: 5.2% × (1 – 0.37) = 3.28% after-tax

- Municipal fund: 3.8% (tax-free) = 3.8% after-tax

The municipal fund won by 0.52%, which on a $50,000 balance meant an extra $260 per year.

Quick Tax Brackets for 2024:

- 22% bracket: $47,151 – $100,525 (single)

- 24% bracket: $100,526 – $191,050 (single)

- 32% bracket: $191,051 – $364,200 (single)

If you’re in the 24% bracket or higher, definitely run the after-tax math on municipal funds.

The Compound Effect of Reinvesting Distributions

Most people don’t realize that money market funds pay distributions monthly, and what you do with those payments matters more than you’d think.

I tracked this religiously in 2023 with my own investments:

$25,000 in SPAXX, reinvesting distributions:

- Month 1: $25,000 × 4.2% ÷ 12 = $87.50 distribution

- Month 2: $25,087.50 × 4.3% ÷ 12 = $89.81 distribution

- Month 3: $25,177.31 × 4.4% ÷ 12 = $92.32 distribution

After 12 months:

- With reinvestment: $26,127

- Taking distributions as cash: $25,000 + $1,087 = $26,087

- Difference: $40 in extra compound growth

That might not seem like much, but over multiple years it adds up. On a $100,000 balance, that same effect would generate an extra $160 annually.

Pro Tips for Maximizing Compound Growth:

- Set up automatic reinvestment (most brokers offer this free)

- Don’t check your balance daily – let the compounding work

- If you need some cash flow, reinvest 80% and take 20% as income

- Consider tax-loss harvesting if you have multiple money market positions

The key insight I’ve learned is that money market funds aren’t just parking spots for cash – they’re tools that require some strategy to maximize. The difference between a thoughtless approach and a strategic one can easily be hundreds of dollars per year, even on modest balances.

Conclusion

After years of working with money market funds both personally and professionally, I’ve come to realize they’re one of the most underutilized tools in the average investor’s toolkit. The financial industry doesn’t promote them heavily because there’s not much profit margin, but that’s exactly why they’re so valuable for you and me. While they won’t make you rich overnight like some flashy investment might promise, they provide something arguably more important: consistent, reliable returns on cash you need to keep accessible.

The biggest mistake I see people make is treating all money market funds like they’re identical – they’re not. Taking the time to understand the differences between government, prime, and municipal funds, along with doing some basic homework on expense ratios and holdings, can easily add hundreds or even thousands of dollars to your returns over time. It’s not glamorous work, but neither is losing money to inflation while your cash sits in a 0.50% savings account when quality money market funds are yielding 5%+.

Disclaimer: This content is for educational purposes only and should not be considered personalized financial advice, as money market fund performance can vary and past results don’t guarantee future returns. Please consult with a qualified financial advisor before making investment decisions, especially regarding tax implications and risk tolerance that may be specific to your individual situation.