Real-Time Payments vs Traditional: The Shocking Truth

Real time payments recorded 266.2 billion transactions globally in 2023, with transaction volumes growing by 42.2% year-over-year and expected to continue strong growth through 2025. As a corporate banker who has been working in this space since 2022, I’ve witnessed firsthand the dramatic transformation of payment infrastructure and client expectations around instant money movement. While traditional wire transfer services once dominated the landscape, real-time payments with the right personal banking services are now reshaping how financial institutions serve their clients.

When I started my banking career, real-time payments were still considered a specialized product offering, but today they’re becoming table stakes for competitive commercial banking. This comprehensive guide provides banking professionals and business clients with essential insights into real-time payment systems, from technical infrastructure to strategic implementation considerations.

Key Benefits of Real Time Payments for Banking Clients

From a product perspective, real-time payments address several critical pain points in traditional payment processing that directly impact business operations and financial performance. Understanding how payment timing affects cash flows and risk management is essential for evaluating these solutions from a banking perspective.

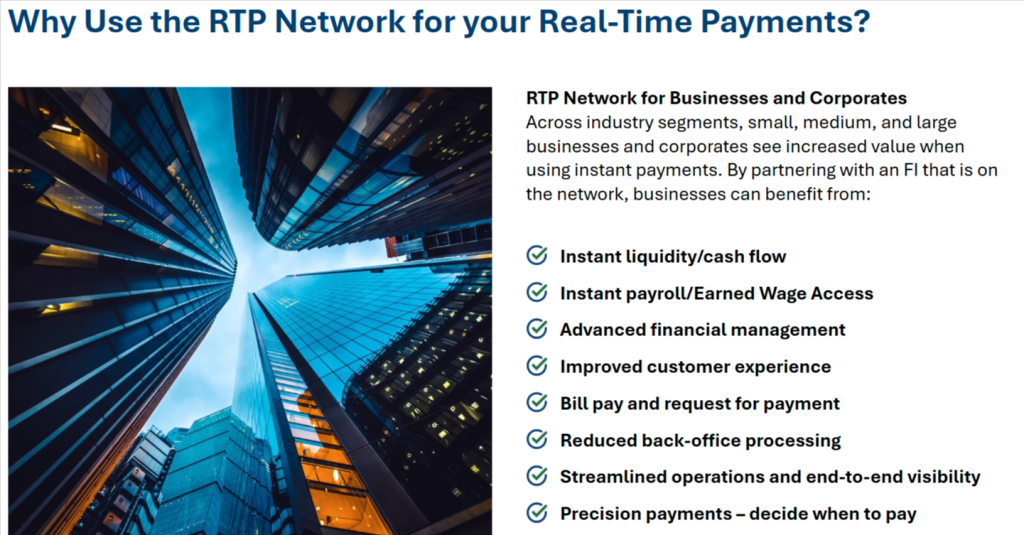

Operational Efficiency The 24/7 processing capability addresses a critical gap in traditional payment infrastructure, particularly valuable for businesses with loan repayments or time-sensitive supply chains. Manufacturing companies can avoid production delays through instant supplier payments, while service businesses can improve customer satisfaction through immediate payment confirmations.

Risk Management Enhancement Real-time payments provide immediate fund verification and irrevocable settlement, eliminating the uncertainty period characteristic of ACH processing where returns can occur up to 60 days after initial settlement. This immediate finality provides operational certainty crucial for high-risk transactions or new trading partner relationships.

Competitive Differentiation Market surveys consistently show that businesses offering real-time payment options achieve higher customer retention rates and premium pricing capabilities compared to competitors using traditional payment methods, with companies like Lyft and Upwork using RTP for instant gig worker payments and AirBnB leveraging RTP for immediate host payments with enhanced transaction data to differentiate their platforms. This competitive advantage becomes increasingly important as client expectations evolve toward instant service delivery, particularly as 61% of businesses now expect competitive advantages from real-time payment capabilities.

Understanding Real Time Payment Limitations and Risk Considerations

Banking professionals must clearly communicate inherent limitations and risk factors to ensure appropriate client expectations and risk management protocols.

Irrevocability Risk The irreversible nature of real-time payments represents the most significant operational risk and a key reason why many companies continue to rely on traditional payment methods. Unlike ACH transactions, which allow for returns and corrections within defined timeframes, and wire transfers, which can sometimes be recalled before final settlement, real-time payments cannot be reversed once settled. This fundamental limitation makes some businesses hesitant to adopt RTP, particularly those with complex vendor management processes or higher error rates, as they lose the safety net of being able to retract payments made to incorrect recipients. This necessitates enhanced authorization controls and comprehensive payee verification procedures for organizations that do implement real-time payments.

Transaction Limits Current network limits create significant operational burden for large corporations that routinely process transactions worth millions of dollars daily. RTP Network limits of $10 million per transaction and FedNow limits of $500,000 (increasing to $1 million in summer 2025) force these enterprises to fragment large payments into multiple smaller transactions, creating additional processing overhead, reconciliation complexity, and increased administrative costs. This operational burden often makes traditional wire transfers more practical for high-value corporate payments, as companies must either dedicate resources to managing multiple RTP transactions or maintain parallel payment infrastructures to handle transactions exceeding network limits.

Cost Considerations at Scale Real-time payment fees of approximately $0.045 per transaction represent significant increases over typical ACH costs, which range from $0.20 to $1.50 per transaction for standard processing. For businesses processing thousands of routine payments monthly, this cost differential can compound substantially – a company processing 10,000 monthly payments would face approximately $450 in RTP fees compared to $2,000-$15,000 in ACH fees, making the absolute cost comparison more complex when factoring in the operational benefits and reduced processing time of real-time payments. However, businesses must carefully weigh these direct transaction costs against the additional infrastructure, integration, and risk management expenses required to implement RTP systems at scale.

Network Fragmentation The lack of interoperability between RTP and FedNow networks creates operational complexity and limits payment reach. Businesses must often maintain relationships with multiple banks or accept coverage limitations that can affect payment strategy effectiveness.

The Competitive Landscape: RTP Network vs FedNow

Observing market developments since the FedNow launch on July 20, 2023, provides insights into how these competing networks are reshaping the payments landscape from both a product and market structure perspective.

RTP Network Foundation The RTP Network, operated by The Clearing House (owned by major banks like JPMorgan, Bank of America, and Citi), established early market presence starting in 2017. The network’s bank-owned structure provided stability and industry alignment while creating participation barriers for smaller financial institutions. RTP processed 343 million transactions in 2024 with $246 billion in payment value, representing a 94% increase from the previous year.

FedNow Market Impact FedNow’s entry fundamentally altered competitive dynamics. The Federal Reserve’s competing network addressed market concentration concerns and accessibility issues. FedNow offers strategic advantages including lower participation costs, standardized connectivity requirements, and explicit regulatory support for broader adoption.

The rapid FedNow adoption rate has been remarkable, with over 900 financial institutions enrolling within the first year, including many community banks and credit unions that couldn’t economically access RTP. This expansion dramatically increases the addressable market for real-time payments.

Strategic Considerations Network interoperability remains the critical missing piece. Both networks are exploring technical solutions, but regulatory and competitive considerations complicate progress. Banking professionals must assess client needs against network coverage when developing payment strategies.

Supporting both networks provides maximum client utility but doubles infrastructure investment and operational complexity. Many banks are taking phased approaches, prioritizing the network that best serves their core client demographics while planning eventual dual-network support.

Implementation Strategy and Advisory Approach

Banking professionals should guide clients through real-time payment adoption using a structured approach that ensures successful outcomes and appropriate risk management.

Assessment Framework Initial evaluation requires comprehensive analysis of payment volumes, timing requirements, and cost sensitivity. Transaction analysis should identify payments that would benefit most from real-time processing, including supplier payments with early-pay discounts, emergency vendor payments, and customer refunds requiring immediate processing.

Treasury Integration Real-time payments require different cash management approaches compared to traditional ACH processing. Businesses must establish appropriate account structures, funding mechanisms, and liquidity management protocols to support instant settlement requirements.

Risk Control Implementation Enhanced authorization workflows, transaction monitoring systems, and fraud detection protocols become essential given the irrevocable nature of real-time payments. Graduated authorization levels based on payment amounts and beneficiary verification status are recommended.

Technology Integration Integration complexity varies based on existing systems and payment volumes. Enterprise clients often require API-based integration with treasury management systems, while smaller businesses may rely on enhanced online banking interfaces. Pilot programs with limited transaction types are recommended before full-scale implementation.

Performance Monitoring Ongoing performance monitoring and optimization require quarterly reviews of real-time payment usage, cost analysis, and exception handling to ensure continued alignment with business objectives.

Future Outlook and Strategic Considerations

The real-time payments landscape will continue evolving rapidly, driven by regulatory initiatives, technological advancement, and competitive pressures.

Network Evolution Network consolidation or interoperability solutions will likely emerge within the next 24 months. Regulatory pressure and client demand for seamless real-time payment capabilities will drive technical solutions enabling cross-network transactions.

International Connectivity Cross-border real-time payments represent the next major expansion opportunity. Early initiatives connecting US networks with international systems like the UK’s Faster Payments or Canada’s Real-Time Rail are under development.

Enhanced Capabilities Request-for-payment capabilities, attached payment messages, and integration with digital identity verification systems will expand real-time payment utility beyond simple fund transfers, enabling new business models and operational efficiencies.

Regulatory Environment The Federal Reserve’s active involvement through FedNow demonstrates commitment to competitive, accessible real-time payment infrastructure. Additional regulatory initiatives addressing network access, pricing transparency, and risk management standards are likely.

Bottom Line?

The transformation of America’s payment infrastructure through real-time processing capabilities represents one of the most significant developments in commercial banking since the introduction of electronic payments. From a banking product perspective, it’s clear that businesses implementing strategic real-time payment programs can achieve measurable improvements in cash flow management, operational efficiency, and competitive positioning.

The dual-network environment created by RTP and FedNow, while initially complex, ultimately provides banking professionals with unprecedented flexibility to design payment solutions that precisely match client requirements. Looking ahead, the continued expansion of real-time payment capabilities will fundamentally reshape how businesses approach treasury management, supplier relationships, and customer service delivery.