Tax-Free Municipal Bond ETFs: Complete Guide for Beginners

High earners in the top tax bracket can keep up to 40% more of their bond income by choosing municipal bonds over taxable alternatives. In 2025’s complex tax environment, tax-free municipal bond ETFs have become the secret weapon for wealthy investors looking to maximize their after-tax returns.

Muni bond ETFs aren’t just for the ultra-wealthy anymore—with tax rates potentially rising and new legislative changes on the horizon, even middle-income investors are discovering the power of tax-free income. Whether you’re in the 22% tax bracket or paying the top rate of 37%, understanding how tax-free municipal bond ETFs can supercharge your portfolio is absolutely crucial.

What Are Tax-Free Municipal Bond ETFs?

I’ll be honest – I was initially puzzled why anyone would choose municipal bond ETFs over regular short-term bond ETFs. The benefits weren’t obvious, and Treasuries seemed simpler. My introduction came through a client who wanted munis, making me wonder why they wouldn’t just buy corporate bonds for higher yield or Treasuries for safety. That’s when I learned there’s strategic importance for both issuers and buyers – it’s a deliberate financial strategy benefiting both sides, not an arbitrary choice.

Municipal bond ETFs are basically investment funds that hold a bunch of municipal bonds – those are bonds issued by cities, states, and other local government entities. Think of it like a basket filled with IOUs from different municipalities across the country. Instead of buying individual bonds from, say, the city of Phoenix or the state of California, you’re buying shares in a fund that owns hundreds or even thousands of these bonds.

The real magic happens with the tax treatment. The interest income from municipal bonds is typically exempt from federal income taxes. And here’s where it gets even better – if you live in the same state that issued the bonds, you often don’t pay state taxes on that income either. This tax-free interest income is very important because even if you park your money in high yield savings accounts like Marcus Goldman Sachs, they will still apply tax on it. For example, if you’re living in NYC:

- Marcus savings account pays 3.65% APY, but you’d owe taxes on that interest

- Federal taxes: up to 37%

- New York state taxes: up to 10.9%

- NYC taxes: up to 3.876%

But with Vanguard’s New York Tax-Exempt Bond ETF (MUNY), a NYC resident would avoid all three layers of taxation. To illustrate this difference with $10,000 invested:

Marcus Savings Account:

- Annual interest earned: $365 (3.65% APY)

- Combined taxes owed: $130 (34.67% total tax rate)

- After-tax income: $245

NY Municipal Bonds:

- Annual interest earned: $320 (3.2% yield)

- Taxes owed: $0 (completely tax-free)

- After-tax income: $320

Tax Savings:

- Annual tax savings: $130

- 10-year tax savings: $1,300

- Plus $75 more annual income ($320 vs $245 after-tax)

Two Main Types of Muni-Bond ETFs

There are two main types of municipal bonds you’ll find in these ETFs. General obligation bonds are backed by the full faith and credit of the issuing municipality – basically their ability to raise taxes to pay you back. Revenue bonds, on the other hand, are backed by specific revenue streams like toll roads, airports, or water systems.

I tend to prefer the revenue bond variety because they’re similar to asset-backed securities – they have dedicated cash flows from specific assets or projects backing them. This gives you a more direct connection to the underlying economic performance of the asset. With revenue bonds, you’re essentially investing in the cash-generating ability of specific infrastructure projects rather than relying on a government’s general taxing power.

Advantage of Investing in Muni-Bond ETFs – Liquidity

One huge advantage of going the ETF route versus buying individual municipal bonds is liquidity, and this is where ETFs really come in handy. The vast majority of municipal bonds are not traded on a regular basis, so the market for a specific municipal bond may not be particularly liquid, and this lack of liquidity and high search costs are reflected in mark-ups on muni trades that are often orders of magnitude larger than similar trades in corporates or equities. Individual municipal bonds suffer from a fragmented and thinly traded nature of the market, making selling prior to maturity a challenge for municipal bond investors.

This is exactly where municipal bond ETFs shine. Bond ETFs provide investors with intraday liquidity, allowing them to buy or sell shares throughout the trading day at market prices, and you can sell bond ETFs on the exchange like stocks and receive the sale proceeds immediately. Instead of dealing with wide spreads and hunting for buyers in an illiquid market, ETFs give you the flexibility to make portfolio adjustments instantly during market hours. That liquidity advantage is worth its weight in gold when you need quick access to your money or want to rebalance your portfolio.

Who Should Invest in Municipal Bond ETFs?

In short: Municipal bond ETFs are best suited for investors in the 22% federal tax bracket or higher, where the tax-free income typically beats taxable bonds on an after-tax basis. The advantage is even greater for high earners in high-tax states like California and New York, where combined tax rates can exceed 40%. Lower-income investors in the 10-12% tax brackets should stick with taxable bonds, as should anyone investing in tax-advantaged accounts where the tax benefit is minimal.

Key Formula: Taxable Equivalent Yield

Tax-Free Yield ÷ (1 – Your Tax Rate) = Taxable Equivalent Yield

Scenario: 24% Federal Tax Bracket

- Taxable Bond: 4.0% yield

- Municipal Bond ETF: 3.2% tax-free yield

Step-by-Step Comparison

Taxable Bond After-Tax Yield:

- 4.0% × (1 – 0.24) = 4.0% × 0.76 = 3.04% after taxes

Municipal Bond Taxable Equivalent:

- 3.2% ÷ (1 – 0.24) = 3.2% ÷ 0.76 = 4.21% equivalent

Result: Municipal bond wins (3.2% tax-free vs 3.04% after-tax)

Tax Bracket Comparison Table

| Tax Bracket | Taxable Bond (4%) After-Tax | Muni Bond Breakeven Yield | 3% Muni Equivalent Yield |

| 12% | 3.52% | 3.52% | 3.41% |

| 22% | 3.12% | 3.12% | 3.85% |

| 24% | 3.04% | 3.04% | 3.95% |

| 32% | 2.72% | 2.72% | 4.41% |

| 35% | 2.60% | 2.60% | 4.62% |

| 37% | 2.52% | 2.52% | 4.76% |

State Tax Impact (High-Tax States)

California Example (37% Federal + 13.3% State = ~44% Combined)

- Taxable Bond: 4.0% → 2.24% after taxes

- CA Muni Bond: 2.5% tax-free → 4.46% equivalent yield

- Advantage: 2.5% vs 2.24% (municipal bond wins by 0.26%)

New York Example (37% Federal + 8.82% State = ~41% Combined)

- Taxable Bond: 4.0% → 2.36% after taxes

- NY Muni Bond: 2.8% tax-free → 4.75% equivalent yield

- Advantage: 2.8% vs 2.36% (municipal bond wins by 0.44%)

Quick Decision Rules

Municipal Bonds Make Sense When:

- You’re in the 22% federal tax bracket or higher

- You live in a high-tax state (CA, NY, NJ, etc.)

- Municipal bond yield × your tax savings > comparable taxable bond after-tax yield

- You don’t need the money for at least 3-5 years

Stick with Taxable Bonds When:

- You’re in the 10-12% tax bracket

- Municipal bond yields are significantly lower than taxable equivalents

- You’re investing in tax-advantaged accounts (401k, IRA) where tax benefits don’t matter

Real-World Yield Comparison (as of recent market conditions)

| Investment Type | Typical Yield | After-Tax (24% bracket) | After-Tax (37% bracket) |

| 10-Year Treasury | 4.50% | 3.42% | 2.84% |

| Corporate Bonds | 5.20% | 3.95% | 3.28% |

| High-Grade Muni ETF | 3.80% | 3.8% (tax-free) | 3.8% (tax-free) |

| High-Yield Muni ETF | 4.50% | 4.5% (tax-free) | 4.5% (tax-free) |

Who benefits most:

- Taxpayers in 22%+ federal brackets

- High-income earners in high-tax states

- Investors with 3-5+ year time horizons

- Those seeking steady, tax-advantaged income

Who should skip them:

- Lower tax bracket investors (10-12%)

- Money needed within 1-2 years

- Investments in tax-advantaged accounts where the tax benefit is wasted

The math is clear: once you hit middle-to-upper income tax brackets, municipal bond ETFs often provide superior after-tax returns compared to taxable bonds.

Current Popular Muni-bond ETFs:

Key Details:

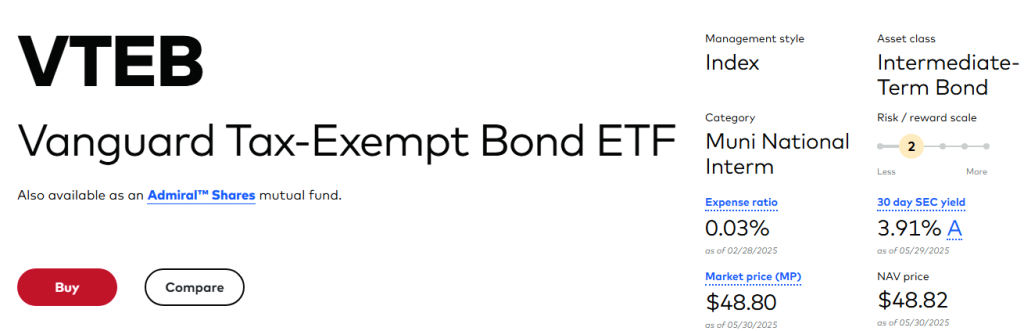

- VTEB: 0.03% expense ratio, 30-day SEC yield of 3.61%

- VCRM: 0.12% expense ratio, actively managed

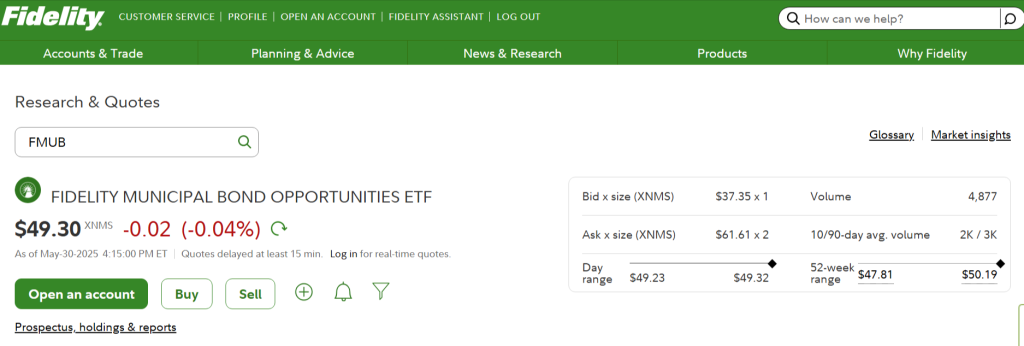

- Fidelity – Best Municipal Bond ETFs

2. Fidelity – Best Municipal Bond ETFs – Fidelity recently launched two new municipal bond ETFs in 2025: the Fidelity Municipal Bond Opportunities ETF (FMUB) and the Fidelity Systematic Municipal Bond Index ETF (FMUN). FMUB is actively managed with a 0.30% expense ratio, while FMUN is passively managed with a 0.05% expense ratio.

Key Details:

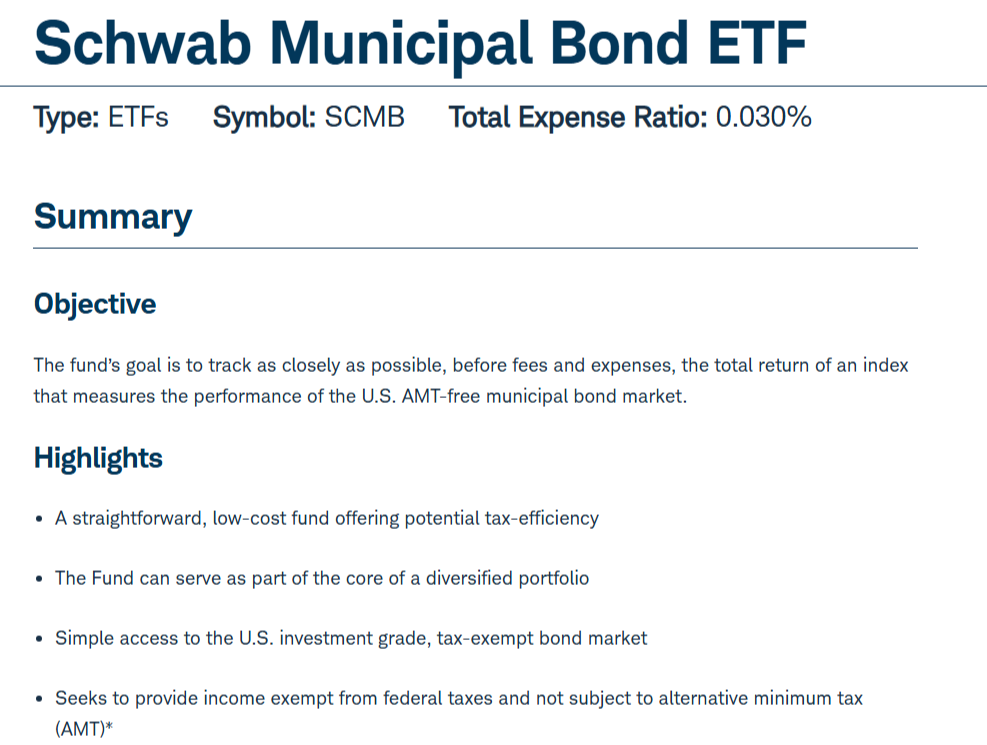

3. Schwab Municipal Bond ETF (SCMB) – This fund tracks the ICE AMT-Free Core U.S. National Municipal Index and provides broad access to the U.S. investment-grade, tax-exempt bond market. The fund seeks to provide income exempt from federal taxes and not subject to alternative minimum tax (AMT).

Key Details:

- Core portfolio holding suitable for diversified portfolios

- Low-cost, straightforward approach

- AMT-free municipal bonds

4. iShares National Muni Bond ETF (MUB) – This is BlackRock’s flagship municipal bond ETF and the largest U.S.-listed municipal bond ETF currently trading with $39.2 billion in assets. It has a 0.05% expense ratio and Morningstar Silver rating iShares National Muni Bond ETF | MUB – BlackRock. BlackRock also recently expanded its municipal bond ETF suite with the iShares Long-Term National Muni Bond ETF (LMUB) with a 0.09% expense ratio.

Key Details:

- MUB: 0.05% expense ratio, largest muni bond ETF

- LMUB: 0.09% expense ratio, long-term focus

- MEAR: Short maturity municipal bond active ETF

Conclusion

Tax-free municipal bond ETFs represent one of the most powerful tools available for tax-conscious investors in 2025. The combination of steady income, tax advantages, and professional management makes these ETFs particularly attractive for high earners looking to optimize their after-tax returns. Remember, it’s not what you earn—it’s what you keep that counts!

Disclaimer: The analysis in this article uses simplified calculations based on publicly available tax rates and interest rates for illustrative purposes only. Actual tax implications will vary based on your specific income level, filing status, and other factors. Please consult with a tax professional for advice tailored to your situation.